Energy Sector Macro Review (Part 2)

The Tariffs And What Energy Investments Make Sense

By: Jon Costello

This is the second part in a four-part review of the energy sector's current macro setup.

Investors trying to make sense of the tariff situation are forced to delve into the highly polarized political realm and all the passions it ignites. In the following discussion of the situation, I’ve done my best to remain objective and to weigh both sides equally. Unfortunately, I don’t emerge much less confused, but I have an approach for managing the potentially fearful environment that may unfold.

Turning first to the tariff situation, as I see it, there are two takes: one positive take that sees the logic in Trump’s actions and one negative, which views his actions as more or less crazy. I present both in what follows before discussing my own take and implications for investing.

The Positive Take on Tariffs

Here is my version of the positive take:

Trump’s no genius, but he’s not dumb, either. After all, he single-handedly mounted one of the most spectacular political comebacks in recent memory. His political instincts are sharp, and he understands that if his poll numbers fall low enough, he’ll risk losing the Republican majority in next year’s mid-terms. If the Republicans lose the House and Senate, Trump’s power will be significantly reduced. Therefore, he has to act on this issue now—and quickly—while he has time to negotiate and endure whatever economic turbulence awaits over the next few quarters.

There is sound logic behind the tariff mess. The huge cloud of dust Trump kicks up through his erratic signaling is another negotiating tactic. It serves to heighten fear during negotiation in the near term so fear can be alleviated after terms are agreed. The ultimate outcome can then be viewed as a “win.”

There are five discrete categories of tariffs, each of which serves a different purpose:

Automobile tariffs on Mexico, Canada, and Germany. Mexico and Canada will be dealt with through a roll-forward of the USMCA agreement currently scheduled for 2026. Germany charges the U.S. 10% tariffs, so the blanket 10% U.S. tariffs already address the issue. The remaining issues will be negotiated relatively quickly.

Reciprocal tariffs. These are the main “sticks” in the negotiations. They also serve the convenient purpose of exposing the hypocrisy of countries that complain about the U.S. tariffs. These are likely to be delayed if there is progress on other fronts with other countries.

Ten Percent blanket tariff.This is more the meat of the tariff issue. These tariffs are intended to boost government revenue and incentivize the return of manufacturing. The 10% is a starting gambit for an across-the-board tariff rate that settles in around the mid-single-digits percent.

Tariffs on China. This is a unique situation that will take the most time. Trump is likely to relent on them once he sees China is willing to talk. These tariffs are the biggest unknown. What is known is that negotiations will be drawn out and the range of potential outcomes is wide. They will also cover far more ground than negotiations with other trade partners. This is why news about China-U.S. tariffs causes such pangs of angst/relief in financial markets as events unfold.

By the second half of the year, most of these tariffs will be gone. Trump is not intentionally looking to cause a recession. Rather, he seeks to establish a legacy as a populist who fought for the common citizen who, for decades, got the raw end of the deals that established the existing international order.

The Negative Take

Next is my version of the negative take:

Trump is a moron. As Charlie Munger claimed, he lacks the characteristics that befit a proper U.S. president. While he may have good political instincts, he doesn’t know anything about economics. In fact, he demonstrates his ignorance every time he speaks about the purpose of tariffs and their impact on the U.S. economy.

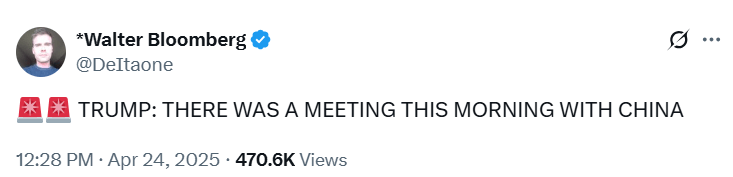

Trump is also a liar. Just yesterday, he said that the U.S. was meeting with China:

Source: @DeItaone, X, April 24, 2025.

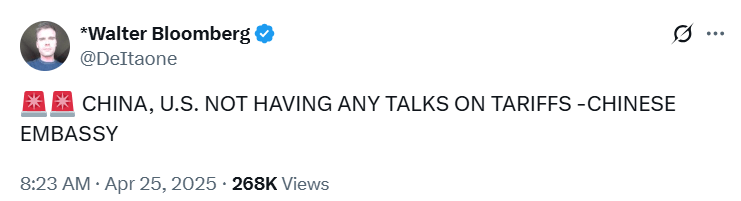

But China then denied any such talks occurred with Trump or any other U.S. government official:

Source: @DeItaone, X, April 25, 2025.

Trump talks a good game about making deals—whether with South Korea, Japan, India, or others—but has nothing to show for it. The situation therefore hasn’t changed at all since “Liberation Day,” despite his attempts to obfuscate reality and claim success where there is none.

Trump will only budge on tariffs if something breaks. It could be an economic or financial market incident. A large-scale event that shocked the economy and/or financial markets would raise the risk that Trump will go down in history as the president who caused a second Great Depression. Only then will reality overcome his egoic commitment to the present course.

Moreover, he may continue to escalate trade issues until he forces a major shock. Once the shock occurs, he’ll roll back all sanctions at once and blame the unfortunate outcome on someone else.

My Take

The above is simply meant to be a sketch of what I understand through my own reading and various conversations. The detailed positions on both sides are more nuanced than the caricatures sketched above, of course. I simplified for the sake of brevity.

But there is clearly a sharp schism between how the two opposing camps interpret the same facts: Trump-as-populist-warrior vs. Trump-as-self-aggrandizing-megalomaniac.

Where do I stand in all this? Even trying to be as objective as possible, I admit to being befuddled.

I don’t think Trump is a moron. But he clearly hasn’t demonstrated a solid grasp of economics. His advisors can come across as buffoonish, and his administration—including the Department of Commerce, which is involved in setting tariff policy—isn’t even fully staffed. It’s no surprise that progress to date has been slow, in stark contrast to the rapid-fire manner in which tariffs were announced and imposed.

I think Trump is more aware of the risks than his critics give him credit for, but I also think his ego introduces all sorts of potential negatives into the picture. I don’t believe he wants to sink the ship that is the U.S. economy. Even so, his tactics are clearly damaging the near-term economic prospects both in the U.S. and abroad.

For example, consider the 10% across-the-board tariffs. These have only been applied for twenty days since they went into effect on April 5. They’re now reverberating through global supply chains. There’s talk about container ships lining up outside China and trucking activity falling fast in the U.S.

In certain areas I follow closely, these tariffs are already having an effect. In oil & gas, many E&Ps are seeing their costs rise because prices for the tubular steel they use to drill wells are increasing. The primary cause of the price increases is not post-tariff imports. It’s due to domestic manufacturers that have boosted their prices after the tariffs went into effect.

The U.S. is the global marginal oil producer, so events like this one, which push costs higher for all producers at once, increase the cost per barrel of marginal supply. In doing so, they increase the prices of crude oil and refined products for consumers worldwide.

I expect a similar chain of events to play out in other segments of the U.S. economy. Shoppers visiting Amazon, Walmart, or Home Depot will see the price impact firsthand. Sure, manufacturers, exporters, and retailers will eat some of the gross tariff cost, but consumer prices will still experience a sharp jump. I expect prices to undergo a swift increase in the mid-single-digit percentage range. That jump should begin to arrive in the U.S. around June.

Higher costs for consumers and lower margins for businesses will reduce ever-important consumer spending and spur layoffs among private sector firms. These private-sector layoffs will add to those taking place in government.

Meanwhile, inflation could push bond yields higher, depressing asset prices and slowing economic growth further. Without a swift reversal over the coming weeks, a recession seems all but inevitable.

All that said, I don’t expect the tariffs to be permanent. One way or another—whether through deals or a sudden reversal—I expect most of them to be gone well before the end of this year. As they’re repealed, Trump will be able to claim victory.