(Idea) Calumet

Calumet, Inc. (CLMT)—formerly the MLP Calumet Specialty Products Partners, LP—just got news that reduces its downside risk while enhancing its upside return potential.

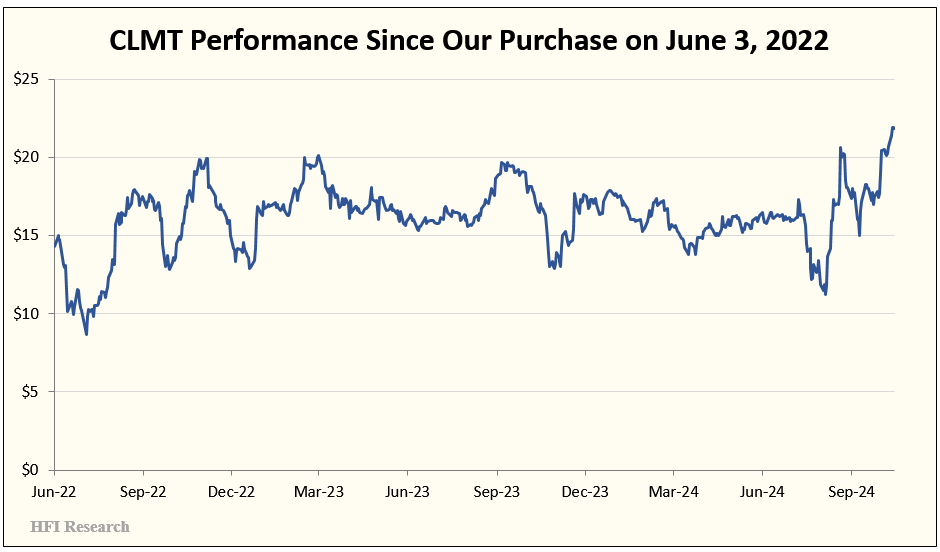

CLMT is the largest position in the HFIR Energy Income portfolio. I originally purchased CLMT units on June 3, 2022, for $14.21 per share. The company doesn’t currently distribute cash to unitholders, but I believed at the time that there was a good chance that distributions/dividends on our purchase price be significant over a multi-year holding period. That remains the case.

I bought CLMT units to diversify our portfolio’s exposure away from oil and natural gas, as the company is primarily a specialty products and lubricants manufacturer. I considered it a special situation, as its fate was tied more to company-specific developments and less to commodity and stock markets.

The “special situation” part of CLMT’s investment thesis is twofold.

First, the company converts from an MLP to a C-corporation. The move is more than just cosmetic. I can’t stress how hated MLPs are among the investing public. CLMT’s conversion to a corporation opens up a whole new world of potential buyers for its stock.

Second, the company is developing a renewable fuel operation called Montana Renewables (MRL). The operation produces sustainable aviation fuel (SAF) and renewable diesel (RD). It is one of the only facilities in North America capable of producing SAF at scale. Moreover, it does so at a low cost by virtue of its favorable location. MRL can source a diverse slate of low-priced feedstock while having access to railways that allow for affordable and flexible transportation options.

I assigned a $30 price target to the shares based on my estimate of value at the time. To say it’s been a wild ride since then is an understatement.

CLMT’s chart is a picture of market inefficiency, which I actually prefer in my investments. The lack of efficiency produced buying opportunities, but it also brought about price moves in the shares that made little sense. Over the course of a month, CLMT would lose 40% of its market value, only to regain all its losses by the end of the month. Sudden drawdowns would occur with enough regularity to make the shares tough to hold—even for a seasoned energy investor.