(Public) CNX Resources - Missing Out On The Natural Gas Bull Market

Hedges all but eliminate the upside price potential.

By: Jon Costello

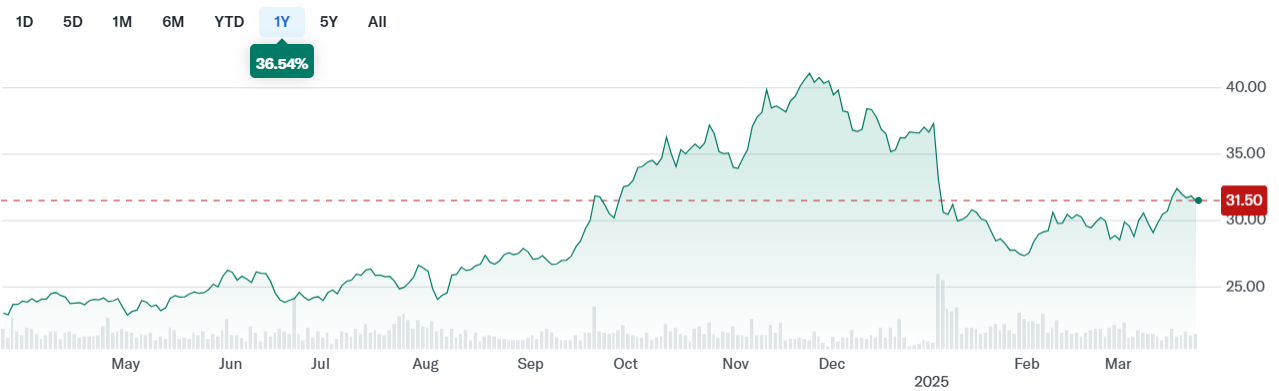

CNX Resources (CNX) shares have been on a wild ride. They’re up 36.5% over the past year, outperforming the broader market but underperforming natural gas E&P peers Antero Resources (AR) and EQT (EQT), which gained 50.8% and 55.8%, respectively, over the same period.

Source: Yahoo! Finance, March 25, 2025.

Unlike AR and EQT, CNX shares have pulled back from their highs late last year, begging the question of whether they’re set to outperform.

The culprit for the recent underperformance was management’s ill-fated decision to bet on the continued rollout of the hydrogen economy. Back in May 2024, the company struck a deal with KeyState Energy and Pittsburgh International Airport to create a sustainable aviation hub that would use CNX’s coal-mine methane (CMM) as a feedstock to produce up to 70 million gallons of sustainable aviation fuel annually. CNX signed a $1.5 billion letter of intent to advance the project.

In the months after the announcement, CNX shares surged by more than 60%, primarily due to the run-up in natural gas prices. During this run, they outperformed both AR and EQT.

Trump’s election marked the turning point.

CNX’s sustainable aviation hub project was dependent on how the U.S. Treasury Department implemented the provisions of the Inflation Reduction Act, specifically, the 45V clean hydrogen production tax credits, from which CNX intended to profit in its airport deal. In guidance announced on January 3, the Trump administration included new restrictions that removed certain economic incentives necessary for CNX to pursue the deal and forced it to back out. In response to the move, its shares fell off a cliff, erasing nearly one-third of CNX’s market cap at its November peak.

The shares have since rallied back in the weeks since their January plunge, but their performance remains far short of peers. While they aren’t overpriced—and are likely to rally further if natural gas prices rise from their current $3.87 per mcf—we believe it’s prudent to avoid them in favor of AR until conditions for CNX improve.

CNX Overview

CNX is a natural gas-weighted E&P operating in the Marcellus and Utica shale basins. The company’s production is 94% gas and 6% liquids, with the liquids comprised almost completely of NGLs. More than 90% of the company’s dry natural gas production is sourced from conventional sources. The remainder is sourced from CMM. Management is guiding to production in 2025 of approximately 1.61 Bcf/d, or 275,000 boe/d.

The company’s production volumes have been fairly steady over the past five years, but volumes are set for a jump after it acquired the natural gas upstream and midstream operations of Apex Energy for $505 million.

CNX’s proved reserve life spans fifteen years at its expected 2025 production rate. However, these reserve figures don’t include those acquired in the Apex acquisition, which closed in January. Apex brought a contiguous block of 36,000 acres that abutted CNX’s own acreage. It also included around 20,000 undeveloped acres in the Marcellus and Utica. The deal is expected to add approximately 185 MMcf/d to CNX’s production in 2025.

CNX realizes a discount on its natural gas sales that can be in excess of 10% of Henry Hub prices. The discount is attributable to the regional oversupply and steep transportation costs in Appalachia. It is partially offset by the relatively high energy content of CNX’s production.

Outside of its upstream activities, CNX earns revenue from operating midstream infrastructure and its “New Technologies” unit, where it receives environmental credits in return for the CMM captured from abandoned coal mines. The company monetizes its carbon capture activities primarily through the Pennsylvania Alternative Energy Portfolio Standard program, in which companies purchase carbon offsets to use toward their own emission goals. In 2025, CNX expects to generate $75 million in free cash flow from 17.5 Bcf of CMM sales volumes, above the $63 million it generated from 18.3 Bcf of CMM sales in 2024.

Natural Gas Hedges: A Tremendous Cash Flow Drag

The main issue with CNX from an investment perspective is the company’s hedging program. CNX hedges more than almost any E&P in North America. The hedges provided a financial benefit over the past two years, when Henry Hub prices traded for long stretches in the $1.80 to $2.50 per mcf range.

However, the hedges will be a severe drag on cash flow over at least the next two years if the natural gas bull market pans out as we expect.

For 2025, CNX hedged a full 85% of its dry natural gas production using fixed-price hedges at an average price of $2.85 per mcf.

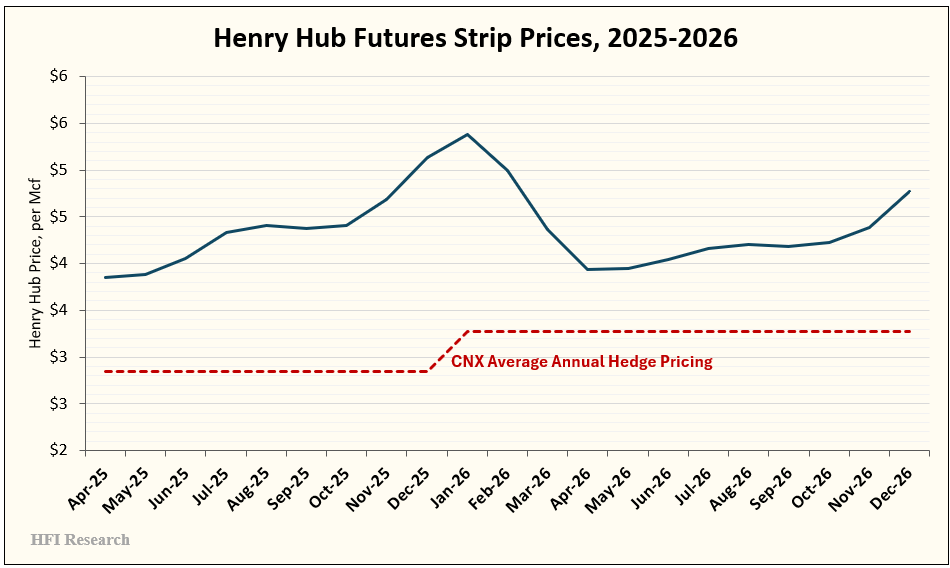

And it gets worse for CNX shareholders who are natural gas bulls. For 2026, CNX hedged another 74% of its dry natural gas production at an average price of $3.27 per mcf, assuming production remains at expected 2025 levels. If prices remain elevated—as we expect they will—the company will realize hedging losses in the hundreds of millions of dollars annually over the next two years. Consider where its hedges stand vis-à-vis Henry Hub strip prices:

Source: CME website, March 25, 2025.

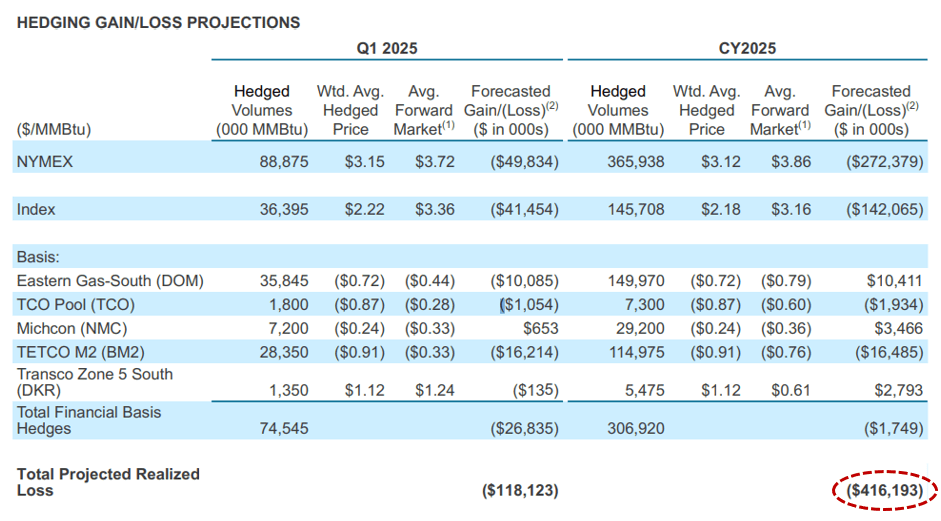

Given the magnitude of volumes involved, CNX itself forecasts a $414 million hedging loss in 2025 from its hedges, as shown in the table below.

Source: CNX Q4 2024 Earnings Supplement, Jan. 30, 2025. Red-dotted line added by author.

The hedging losses include the price discount CNX receives on its production relative to Henry Hub prices. After realized cash losses from hedge settlements, free cash flow is expected to be approximately $500 million.

The extent of CNX’s hedging is perplexing, as the company has no ostensible need for such an extensive hedging program. It’s not exiting or running off its natural gas business; the failure of its airport deal suggests it’ll be committed to its E&P operations for the long term. Its debt is rather high, with $2.1 billion of net debt that is equivalent to 1.8-times cash flow on unhedged production. But debt isn’t at a point that would necessitate hedging 85% of production. After all, higher realized natural gas prices would accelerate debt reduction.

Moreover, CNX has demonstrated that it intends to reduce debt, as it has paid down approximately $100 million annually over the past four years. Additional debt reduction is slated for 2025 and beyond.

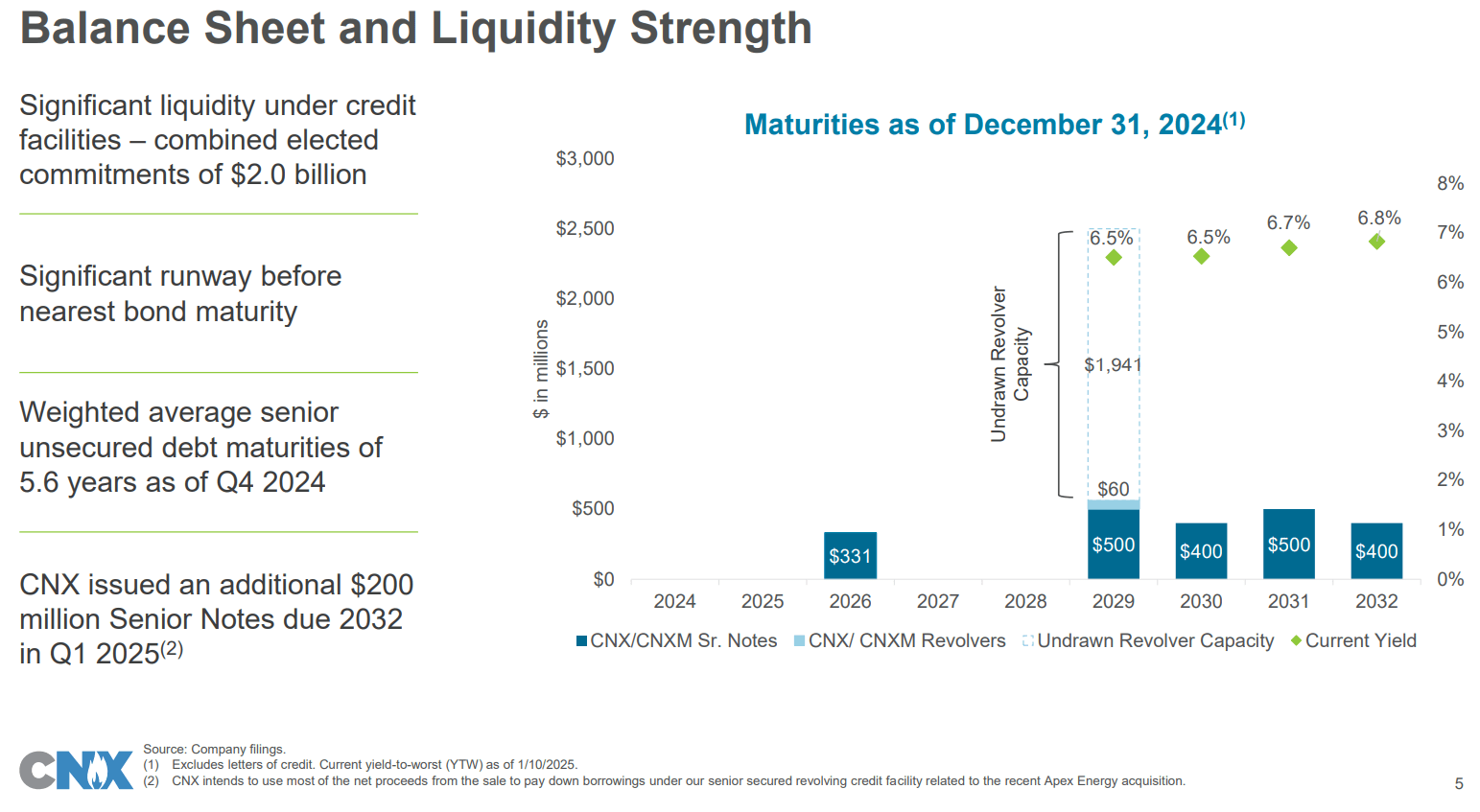

The company’s liquidity is ample, and debt maturities are manageable, as shown below.

Source: CNX Q4 2024 Earnings Slide Presentation, Jan. 30, 2025.

CNX’s hedging program also makes little sense from an operating cost perspective. Like its Appalachian peers, CNX is a low-cost producer in the U.S. It therefore has less need to protect against a sustained bout of low prices than E&Ps with higher operating costs. Its costs are well below those of Haynesville producers. We estimate that on an unhedged basis, CNX’s free cash flow breaks even at a Henry Hub price of approximately $2.35 per mcf with WTI at $70 per barrel, inclusive of corporate costs.

The cash flow drag created by CNX’s hedges severely limits the upside potential in its shares for at least the next two years and likely thereafter unless management’s hedging approach undergoes a major change.

Valuation

Inclusive of hedges and 2025 guidance, we estimate CNX will generate $477 million of free cash flow in 2025, assuming Henry Hub averages $3.50 per mcf and WTI averages $70 per barrel. This level of free cash flow generates a 10.1% free cash flow yield at the current share price of $31.75.

In a bull scenario in which Henry Hub averaged $5.00, the company would generate approximately $600 million in free cash flow, equivalent to a 12.7% yield. Obviously, the hedges significantly reduce the upside potential in free cash flow.

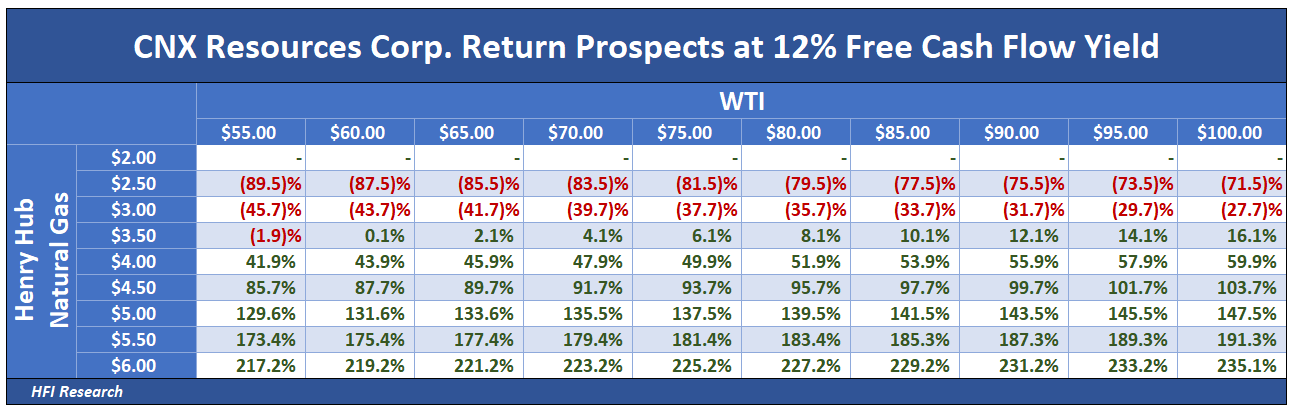

On an unhedged basis, CNX’s return profile is attractive, assuming the shares were to trade at a 12% free cash flow yield. In a natural gas bull market in which Henry Hub is sustained at $5.00 per mcf, CNX would generate a free cash flow yield of 28.3% on its current share price. Its return profile would look as follows.

This is what the company could conceivably achieve in 2027 if natural gas prices cooperate and it refrains from hedging. However, investors banking on such an outcome would have to be confident that management won’t make dumb capital allocation decisions until then. It would be helpful if management clarified its long-term hedging strategy.

It’s tempting to approach this situation as a long-sighted investor, initiating a long around current levels with the intention of holding for a three-to-five-year period. However, CNX’s management introduces enough unknowns into a multi-year holding period to prevent us from considering this strategy. We don’t consider it desirable to partner with a management team that is so risk averse that it feels the need to all but eliminate upside to shareholders if natural gas prices rise. Instead, we’d prefer to hold AR for a three-to-five-year holding period. Range’s management is superior. It is far more directly incentivized to perform for shareholders in all commodity markets. AR has distinguished itself as lower-cost than even CNX and has avoided hedges to capture the upside in a bull market.

If the economy entered a recession and all E&P names were pushed lower, CNX could be an attractive holding if its shares were bought at the low-$20s level. At, say, $25 per share, CNX| would offer a margin of safety and the prospect of multi-bagger returns if its management and board became convinced that the setup for natural gas is attractive enough to remain unhedged. However, the company would have to pay down debt by another $500 million or so to get away with not having to hedge at all.

Additional upside for CNX shares can come from continued share repurchases. In recent years, CNX has spent considerable sums repurchasing its shares. Since 2020, it has reduced its share count by a whopping 36%, from 225 million to 149 million shares. Unlike many other E&Ps, the company’s share repurchases have been concentrated in periods where its shares traded at a wide discount from intrinsic value.

Cash flow upside could also come from favorable rulings or legislation with regard to the various environmental credits it uses in its New Technologies segment.

Conclusion

We’d avoid CNX shares at the moment. AR shares are a superior alternative for natural gas bulls like us. That could change depending on the course of commodity and stock prices. But for the time being, we feel comfortable buying and holding AR while continuing to monitor CNX closely for positive developments.

Analyst's Disclosure: I/we have a beneficial long position in the shares of AR either through stock ownership, options, or other derivatives.