(Idea) New Stratus Energy - A Highly Speculative Name, But Worthy Of A Small Allocation

Warning: NSE shares face a significant risk of permanent capital loss. The shares are illiquid, so buyers must have a long-term thesis and endure inevitable bouts of volatility. The shares should occupy only a small percentage of an investment portfolio. Given their significant upside potential, however, even a 1% weighting could materially move the needle for a portfolio’s overall return if the investment pans out.

NSE Overview

New Stratus Energy (NSE:CA) is a Canadian-domiciled E&P with operations in Latin America. The company ended 2023 with little by way of operations and C$33.1 million of cash. On January 2, 2024, it began to deploy that cash into highly prospective projects.

Our conversation with Wade Felesky, the President of New Stratus Energy, gave us confidence about the integrity of NSE’s operation and, most importantly, the people behind it. We believe the company’s strategy is sound and that it has the assets and personnel necessary to execute over the coming years. What it needs to do next is to demonstrate solid execution, and the next few months will be telling on that score.

NSE’s strategy is to use its deep expertise and extensive roster of contacts in the Latin American energy industry to partner with national oil companies in the development of oil and gas resources. Several Latin American nations lurched leftward over the past decade and, as a consequence, have been starved of capital and expertise necessary to produce anywhere near their capacity.

Recently, however, there have been both subtle—Ecuador and perhaps Mexico—and not-so-subtle—Argentina—shifts toward the center/right. If the shift gains momentum, the time could be ripe for a wider liberalization of the Latin American oil and gas sector. If such a political shift comes to pass, New Stratus is well-positioned to strike deals and execute operationally throughout the South American continent.

Let us state at the outset that the company has a checkered past in terms of execution. In 2018, shortly after CEO Jose Francisco Arata assumed his post, NSE invested millions in an oil production project in Colombia. The project was delayed by Covid, and NSE had to wait for Colombia’s National Agency for Environmental Licenses to complete an environmental study before it could proceed with development. In mid-2022, the agency found that nearly all of NSE’s prospective acreage resided in “highly sensitive” areas that would make development unfeasible. The project was abandoned at a total loss.

Next, NSE tried its hand at producing oil in Ecuador. In January 2022, it invested C$7.2 million to acquire Petrolia Ecuador, which held a 35% interest service contracts in Blocks 16 and 67 in Ecuador. On December 5, 2022, the Ecuadorian government under corrupt President Guillermo Lasso informed NSE that it would not uphold its end of the service contracts for the Blocks. Shortly thereafter, NSE transferred its Ecuadorian assets back to the national government.

On November 23, 2023, Daniel Noboa was elected President of Ecuador. Noboa has vowed to clean up Ecuador’s widespread corruption. At present, NSE has continued to perform decommissioning and environmental audits consistent with the service agreement termination process. Noboa’s arrival gives NSE hope that it can win back the concessions it lost under previous President Lasso. However, we don’t assume that NSE receives any benefit from such an outcome in our analysis.

Management should be given credit for surviving these incidents and emerging with enough cash to purse attractive opportunities. We’re confident its current opportunity set will yield better results.

NSE’s Venezuelan Project

On January 2, 2024, NSE signed an agreement to acquire a 50% interest in GoldPillar International Fund SPE Ltd. GoldPillar is jointly owned by NSE and accomplished businessman Franco Favilla.

GoldPillar is a private company organized under the laws of the British Virgin Islands. It owns a 40% interest in Petrolera Vencupet, S.A., which holds the production rights to six onshore oilfields in eastern Venezuela. A subsidiary of Venezuelan national oil company PDVSA owns the remaining 60% of Vencupet.

The deal is NSE’s first foray into Venezuelan oil production. From a purely macro oil perspective, Venezuela offers attractive opportunities, with an immense base of easily produced oil resources. As shown below, Venezuela’s proved reserves are the largest in the world.

Source: EIA.

If circumstances permit, Venezuela can once again become a key producer of the marginal barrels necessary to meet global demand growth. Its oil is of the heavy variety, which reduces its quality relative to lighter barrels. However, Venezuelan oil offers advantages such as accessibility, low production costs, low decline rates, and access to processing capacity in the U.S. Gulf Coast refinery complex.

Venezuela’s oil and gas industry has suffered from more than a decade of neglect after the flight of capital and expertise. At the moment, U.S. sanctions are further restricting production activity.

The nation’s production has declined from more than 2.5 million barrels per day in 2011 to approximately 700,000 bbl/d today as the socialist government exhausted what remained of the wealth inherited from Venezuela’s once thriving market-based economy.

Source: EIA.

Today, PDVSA is under the control of current President Nicholas Maduro and his United Socialist Party of Venezuela. Political influence and endemic corruption have rendered PDVSA incapable of growing production on its own, so the company is forced to partner with smaller, sanctions-exempt operators like GoldPillar to obtain the capital and expertise required to boost production.

GoldPillar’s Prospects

GoldPillar was organized under the laws of the British Virgin Islands and, as such, is not a U.S. entity. Management has been careful to design the corporation’s ownership, legal, and operational structure so as to avoid running afoul of U.S. sanctions.

While U.S. citizens cannot participate directly in Venezuelan business ventures due to U.S. sanctions, they are permitted to receive passive investment income generated from foreign companies operating in Venezuela. As a Canadian-domiciled company that receives passive income generated in Venezuela, NSE offers one such way for U.S. investors to participate in Venezuelan oil production.

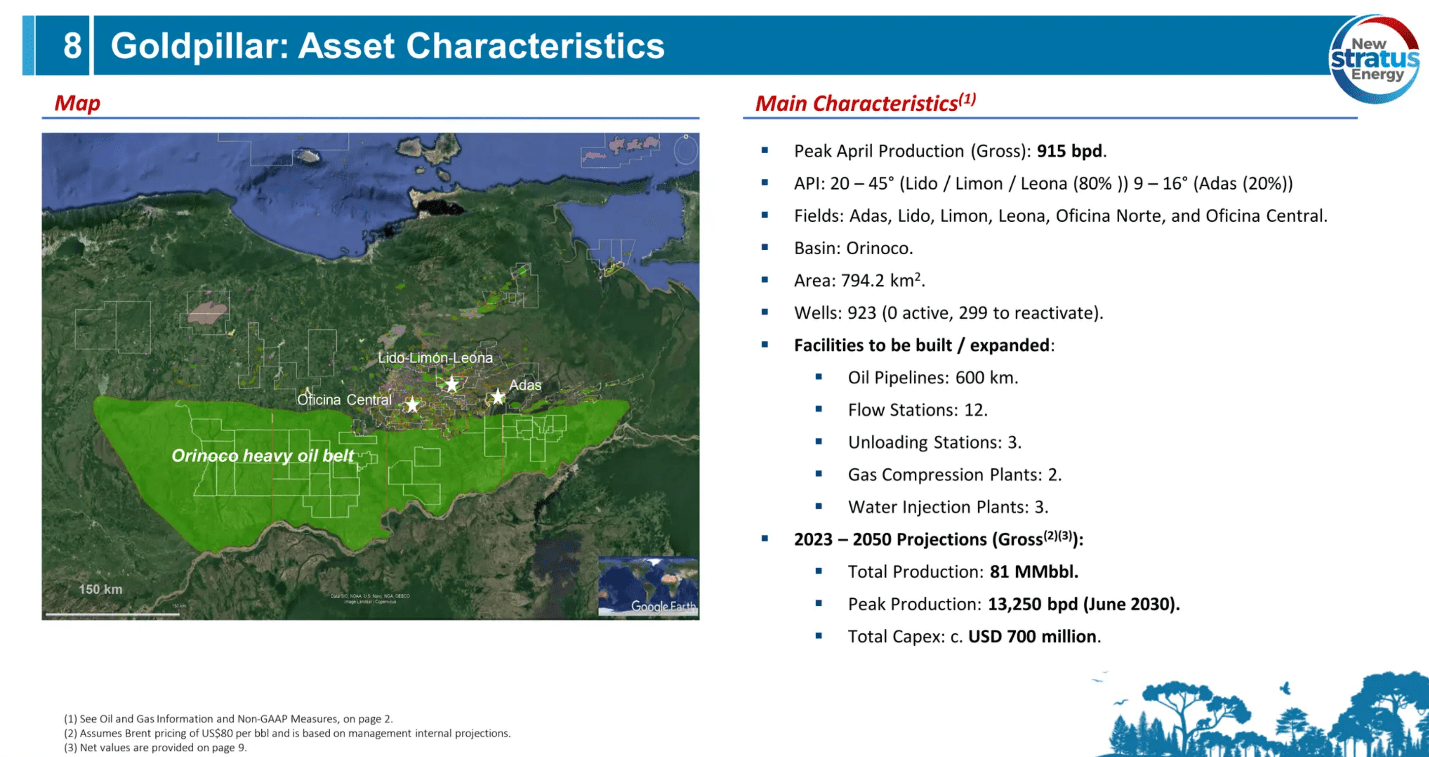

Vencupet’s oilfields are located in a 794.2 square kilometer basin onshore in eastern Venezuela. Their locations are denoted by stars in the map below.

Source: New Stratus Energy May 2024 Corporate Presentation.

Vencupet is in the process of reactivating 90 wells over the course of 2024 and 2025. This process involves returning wells originally drilled in the 1940s through the 1960s to primary production.

Completion data exists for 46 of the 90 wells. Management estimates that 7,400 barrels of oil per day—1,480 net to NSE—can be produced from these wells based on their historical decline curves. After the initial 90 wells have been reactivated, Vencupet plans to reactivate an additional 156 wells on its acreage. Oilfield consultancy Petrotech estimates an 85% chance of successful development in light of the potential for delays, data issues, and supply chain interruptions.

GoldPillar sources revenue from activities other than oil production, which is subject to high levels of taxation. The company also derives revenue from fees associated with trading, operations, and financing. Management expects these other revenue sources to generate significant cash flow net to NSE over the coming years.

To operate in Venezuela, NSE is forced into some idiosyncratic financial arrangements. For one, cash-strapped PDVSA compensates GoldPillar in crude oil instead of currency. Furthermore, NSE cannot directly access cash within Venezuela but can access cash that resides in other global locations. The company can use its cash to repurchase shares, repay debt, and/or pursue new projects.

Despite these idiosyncratic arrangements, NSE management expects Vencupet’s production ramp and its ancillary services to generate significant value over many years for NSE shareholders.

NSE’s Mexican Project

NSE’s second major project is located in Mexico. Mexico’s oil and gas industry has been constrained by the nationalistic policies of its President, Andres Manuel Lopez Obrador. Lopez Obrador’s policies have given Mexico’s national oil company, Pemex, effective control over the nation’s oil and gas markets. As private operators left the country in response to the new regime, Mexico’s oil production has declined. With domestic demand holding steady, its dependence on foreign oil and gas sources has increased.

Lopez Obrador’s chosen successor, Claudia Sheinbaum Pardo, is considered a shoo-in to succeed him when elections are held on June 2. Sheinbaum has pledged to maintain the policies of her predecessor, but she has also promised to downsize Pemex and return it to profitability. These policies could bring about some liberalization of Mexico’s oil and gas sector, which would be positive for the prospects of small operators like NSE.

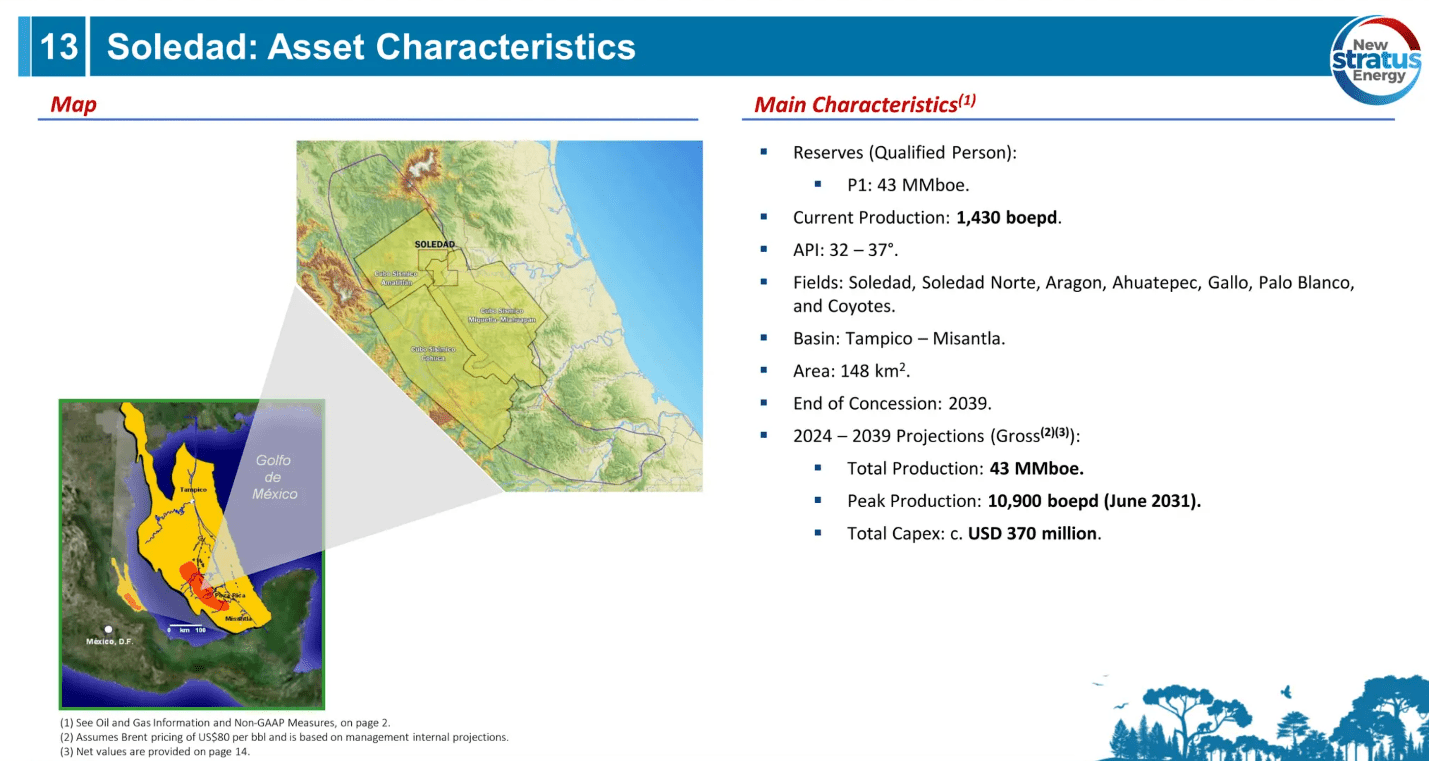

NSE acquired its Mexican operation—officially called “Operaciones Petroleras Soledad S. de R.L. de C.V.,” or Soledad for short—on May 14 of this year. An overview is shown below.

Source: New Stratus Energy May 2024 Corporate Presentation.

Soledad owns a 49% equity interest in a private Mexican oil and gas producer that operates under a contract with Pemex. The first part of NSE’s acquisition of Soledad is expected to close by the end of July, at which point it will be recognized in NSE’s second-quarter results.

Soledad currently produces 1,430 boe/d of oil and natural gas. The project requires more upfront capex to increase production than NSE’s Venezuela project. Management expects to boost production through capex and through the scheduled acquisition of additional equity interests in Soledad over the coming years. NSE’s Soledad ownership stake is expected to step up to 90% in 2026. The increase is expected to drive production growth net to NSE from 2,187 boe/d in 2025 to more than 8,300 boe/d in 2028.

Corporate Governance Issues

Shareholders should be aware that NSE isn’t without some questionable corporate governance practices. On May 30, 2023, it extended the expiration date on 14.05 million warrants by one year. The warrants were exercisable at C$0.45 and set to expire on July 22, 2023, but the extension pushed the expiration date back to July 22, 2024. At the time of the extension, NSE shares were trading well below their exercise price. Had they expired, public shareholders would have avoided significant dilution. Today, the warrants trade in the money with NSE shares at C$0.56.

We firmly favor management being properly incentivized to perform for shareholders. We’re not in favor of compensation goalposts being changed unexpectedly mid-game in a manner that benefits management at the expense of public shareholders.

In addition to warrants, NSE has 11.54 million stock options outstanding with an average exercise price of C$0.41. These options are dilutive to public shareholders, but they provide a strong incentive for management to perform.

Altogether, NSE’s warrants and options increase its share count to 148.5 million shares on a fully diluted basis.

In its latest quarterly filing, NSE disclosed a 1% reduction in its GoldPillar ownership stake. The stake now stands at 49%, down from 50%. The change turns its stake into a minority interest in terms of economics and, presumably, voting rights as well. Management provided scant details on the reasons for the change, other than mentioning that it was associated with the execution of certain documents.

Taking a Stab at a Valuation

As a speculative enterprise that has only recently begun to operate in its current form, we have to rely on management’s forecasts to guide our financial projections. Revenues are projected from anticipated production volumes and expected ancillary service fees. We assume the figures provide an honest assessment of NSE’s financials based on assumed activity levels.

The following table shows our free cash flow estimate for GoldPillar assuming oil prices of $80 per barrel Brent. Recall that NSE owns a 49% interest in GoldPillar, which, in turn, owns a 40% interest in Vencupet, a joint venture between itself and PDVSA. NSE’s net interest in Vencupet’s revenues therefore stands at 19.6%. Our free cash flow estimates reduce the free cash flow figures derived from management’s estimates by 20% to be conservative.

Clearly, the returns on offer from GoldPillar portend massive upside for NSE shares, exclusive of any financial contribution from the Soledad project. Returns approach the 200% mark over the next three-and-a-half years. Of course, returns increase as Brent prices increase due to higher revenues associated with Vencupet’s production volumes and ancillary service fees.

In terms of downside, both Vencupet’s new wells reactivated wells break even at oil prices below $40 per barrel. Adding ancillary fee revenue, we estimate cash flow breakeven to be even lower, far below the breakeven price per barrel for the overwhelming majority of North American oil production.

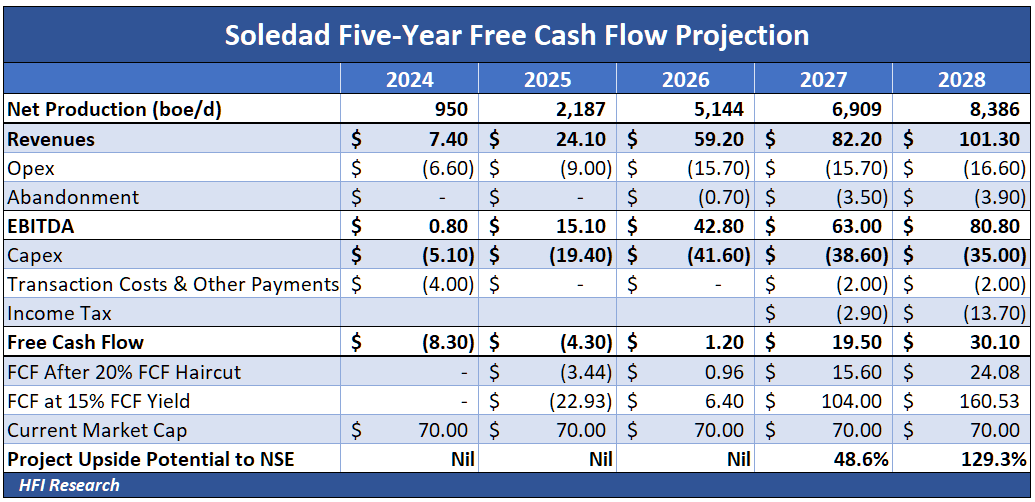

For Soledad, cash flow is projected to be negative over the first few years as it ramps production. Returns improve dramatically thereafter.

Soledad wells offer similar economics to those being drilled by Vencupet in Venezuela.

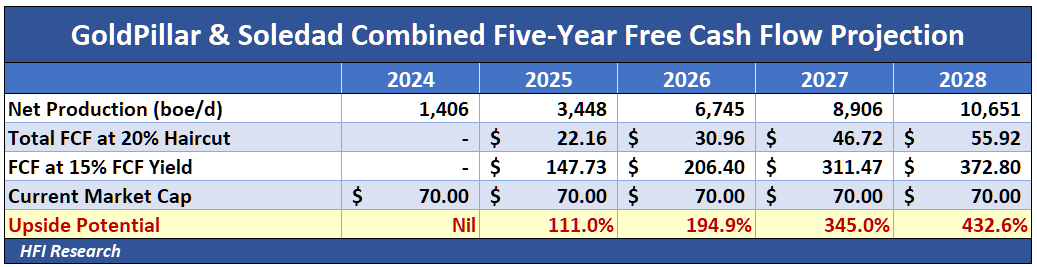

The combined financial impact of GoldPillar and Soledad results in potential multi-bagger returns for NSE shares through 2027.

We’re hard-pressed to find returns remotely as attractive as these in the North American oil patch.

Conclusion

What should current NSE investors look for? In a word, execution. The company’s Venezuelan project is underway, while its Mexican project should begin to contribute to NSE’s financials in the second quarter. Its second-quarter results, scheduled for release in August, will provide an important gauge of the company’s execution and progress.

The recovery of formerly revoked Ecuador service contracts or other compensation from Ecuador’s government could provide additional upside to the shares in the near term.

We view NSE as a worthy speculation. To be sure, risks abound; there are too many unknows to count—asset expropriation, lax or corrupt law enforcement, even war if Venezuela is more than just saber-rattling in its recent threats to Guyana. Due to the clear and present risk in the picture, we believe NSE shouldn’t occupy more than 1% to 2% of an investment portfolio.

That said, bullish factors offset the high risk of loss, namely, the extraordinary upside potential in NSE shares and the rare opportunity to participate in geologically low-risk oil production in Venezuela. Risks aside, it all comes down to management’s execution.

No doubt there are other worthy speculations strewn throughout the global oil patch. In this case, however, our experience with management and our view of the upside makes the risk worth taking.

Analyst's Disclosure: I/we have a beneficial long position in the shares of NSE:CA, GXE.TO either through stock ownership, options, or other derivatives.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Wilson Wang is a director for Gear Energy.