(Idea) Veren Update

Editor’s Note: Since selling VRN for Alibaba back in late August, we have not bought back Veren yet. Jon Costello, head of Ideas from HFI Research and the author of this article, bought Veren on Thursday. Here’s his explanation for why he did that.

We are contemplating another long position in Veren.

By: Jon Costello

Note: Dollar references are to Canadian dollars unless otherwise specified.

Yesterday, I sold our Targa Resources (TRGP) holding to initiate a new Veren (VRN) position in our HFIR Energy Income Portfolio. My objective is to outperform energy income indexes on a price basis while also generating a competitive income yield—both over a period of several years. At our $7.07 purchase price, I expect Veren stock to meet my return requirements.

First off, I believe the time had come to sell TRGP. The shares generated a 319% return over our 45-month holding period, far surpassing my return requirements. They are now approaching overvalued territory, so a switch to a bargain-priced stock made sense.

To be sure, owning such a battlefield E&P stock will make for a rocky ride. Veren’s selloff seems to have no end in sight. The shares are down again today and could fall further. However, over a period of two to three years, I believe their upside is extraordinary. They could appreciate by 100% or more on a total return basis.

The shares are also attractive from an income perspective. Their 6.5% yield on our purchase price exceeds the yields of many midstream corporation stocks.

Veren Taken to the Woodshed

Veren shares have sold off by 28.3% year-to-date. Their weakness over the months has been due to the market’s expectations for a weak third quarter.

Well, yesterday the company delivered—and then some.

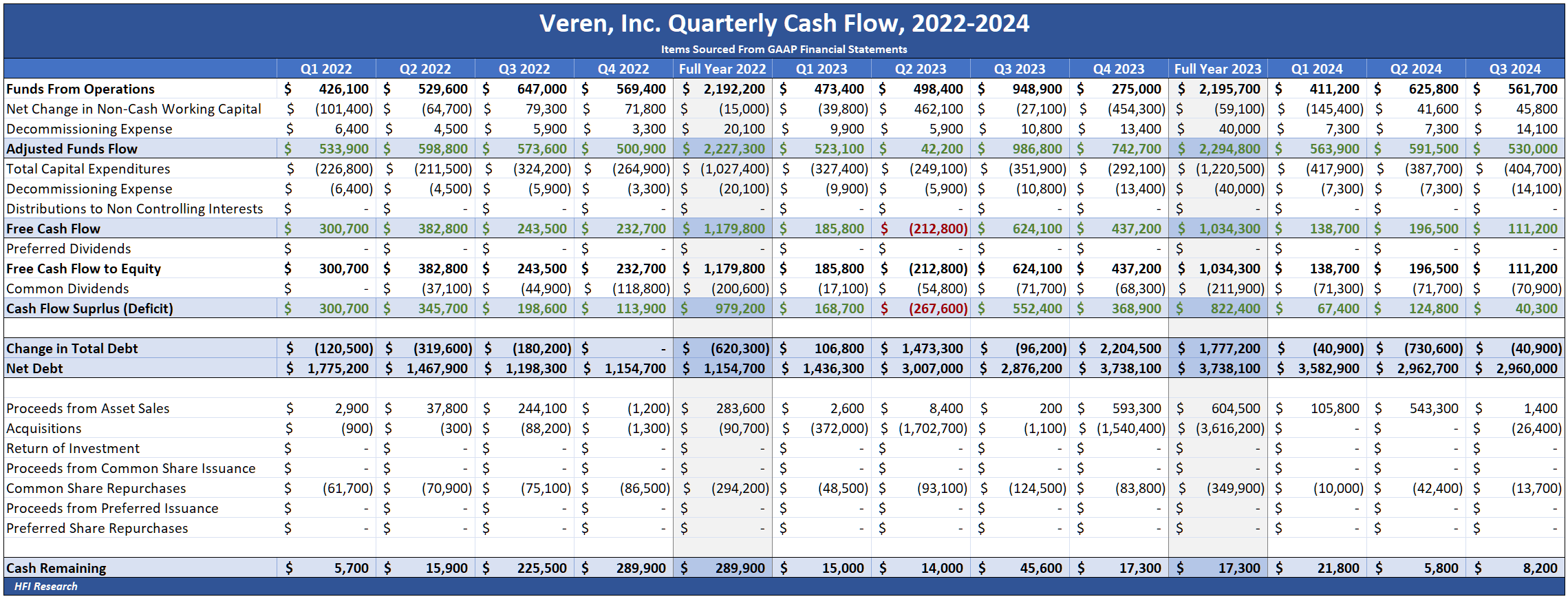

Third-quarter financial results were actually in line with consensus expectations. Free cash flow during the quarter came to $111.2 million, which is positive in light of the heightened capex.

Investor concerns focused on production results and their impact on future financial performance. Production came in at 184,500 boe/d, less than consensus expectations of 190,000 boe/d. The third-quarter miss was attributable to third-party infrastructure outages. These were known in the market and had been priced into Veren shares after their multi-month decline into third-quarter earnings.

Far more alarming were unexpectedly poor production results from wells drilled in October in Veren’s Gold Creek acreage in the Montney.

The well results caused the company to reduce its fourth-quarter production guidance. Consensus expectations for fourth-quarter production results had been around 195,000 bpe/d, but the company’s guidance implies production of 191,000 boe/d. The company also reduced 2025 production guidance from 203,000 boe/d to 192,000 boe/d, or approximately 5%. The lower 2025 guidance caused management to push back the timing of its 5-year plan to grow production to 250,000 boe/d by one year, from 2028 to 2029.

The culprit for the poor drilling result—which rarely occurs to this degree among larger E&Ps—was management’s introduction of a plug-and-perforation, or “plug-and-perf,” well completion design on 11 wells in Veren’s Gold Creek acreage. The design was adopted in an attempt to reduce costs.

The company reported that production from the wells was economic but fell far short of expectations. Since the wells began producing in October, Veren’s production will begin 2025 lower than expected, thereby dragging down full-year results.

The company explained the result in its third-quarter earnings press release.

Source: Veren Q3 2024 Earnings Press Release, Oct. 31, 2024.

Management plans to rectify its mishap by abandoning the plug-and-perf completion design and adopting a single-point entry design instead. Since management initially expected the plug-and-perf design to succeed at reducing drilling capex, its abandonment of the design and adoption of the higher-cost single-point entry design will increase Veren’s capex and reduce its capital efficiency going forward.

While the capital efficiency reduction is real—and will negatively impact 2025 results relative to management’s original expectations—I don’t expect it to significantly reduce Veren’s free cash flow generation over the long term.

In the two days since third-quarter results were announced, Veren shares have sold off by nearly 20% due to the poor drilling results. The magnitude of the selloff indicates the market is concerned that the results were attributable to inferior geology, not completion design. If geology was in fact the culprit, a significant portion of Veren’s Gold Creek acreage could be impaired, raising concerns about its reserve value, cash flow prospects, and equity valuation.

The impairment would occur in a region that Veren considers some of its core Montney acreage. The region is shown circled in red-dotted line in the map below.

Source: Veren October 2024 Investor Presentation. Red-dotted line added by author.

Note that so far, the circled region has been the only one in which Veren has had sub-par drilling results. Its results elsewhere have been strong. Its best wells are among the most productive in the Montney.

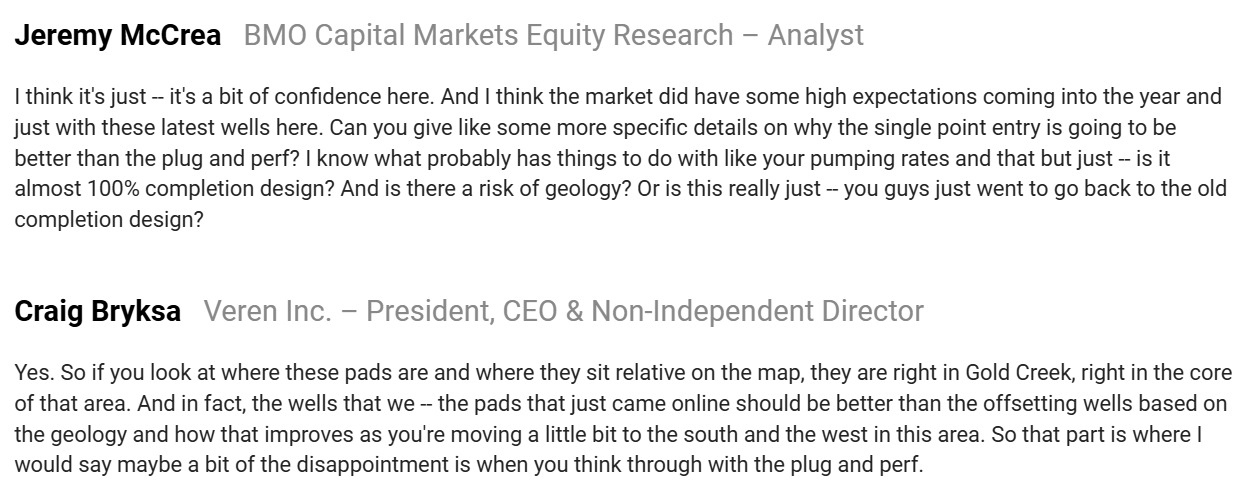

On Veren’s third-quarter earnings conference call, management was firm in stating that the poor drilling result was due to the plug-and-perf completion design, not geology.

Source: BamSEC Veren Q3 2024 Earnings Conference Call Transcript, Oct. 31, 2024.

Clearly, the market doesn’t believe management. That’s the only explanation for the selloff over the past two days. Such a brutal decline reflects the market’s expectations for a significant permanent loss of intrinsic value and cash flow generation.

While we respect the market’s verdict, we’re willing to give management the benefit of the doubt in this case. Despite the non-stop drumbeat of negativity from triumphant Veren bears, some of the most informed market participants we know have high opinions of management, both in terms of strategy and operations. We believe that over the coming quarters, it will rectify its drilling snafu and get production results back on track for 2026 and beyond.

In the meantime, we’ll be content to sit and collect our dividend, which represents an attractive 6.5% yield on our purchase price.