Editor’s Note: This article was first published to HFI Research's main subscribers on Nov 29, 2023. Please note that the market data used in this article will be dated as a result.

Note: Dollar references are to Canadian dollars unless otherwise specified.

Canadian Natural Resources (CNQ) is the largest and best-run E&P in Canada. The company was founded as a junior oil and gas producer in 1988 by Murray Edwards and Allan Markin. Since then, it has expanded primarily through intelligent acquisitions aimed at achieving a diversified, low-cost, and integrated production model. Its management structure is unique among E&Ps, with the company managed by a 22-person committee instead of by a single CEO. Nevertheless, it has demonstrated flexibility and decisiveness when necessary. During the 2014-2020 oil price downturn, CNQ acquired attractive oil and natural gas properties that will benefit its shareholders over the coming years.

The company has few negatives and a long list of positives, which include the following:

Total proved reserve volumes on a scale of international oil majors such as Shell (SHEL), BP (BP), and Chevron (CVX).

32 years of proved reserves at the current production rate, more than double that of CVE and SU.

The lowest corporate decline rate among the large Canadian oil sands companies.

A presence in eight of the ten lowest-cost conventional oil and gas plays in North America.

A dividend that has been paid annually for 23 consecutive years.

A 25% return on capital employed in 2022, one of the highest among large-cap E&Ps.

The highest return on capital employed over the last three years among the large Canadian oil sands companies.

Dividends of $4.34 per share and repurchases of $4.91 per share in 2022.

Planned 2023 production growth of 6% in 2023; 8% on a per-share basis.

At the moment, CNQ is returning 50% of cash flow after current dividends and capex in the form of share repurchases while using any remaining cash flow to pay down debt. Once its net debt is reduced to $10 billion, it plans to return 100% of free cash flow to shareholders as dividends and share repurchases.

CNQ’s Place in a Stock Portfolio

CNQ shares possess less upside to higher oil prices than other oil sands operators like MEG Energy (OTCPK:MEGEF), Suncor Energy (SU), and Cenovus Energy (CVE). For one, CNQ shares trade at a steep multiple to its oil sands peers. As a result, its shares won’t benefit nearly as much as MEG, CVE, and SU from multiple expansion, should it occur. We expect MEG, CVE, and SU to be rewarded with higher multiples as their results improve over the coming quarters and years. Their multiples also have greater room to move higher if the investing public regains confidence in the longer-term outlook for global oil demand. By comparison, CNQ—already renowned for its high quality—has considerably less upside from multiple expansion.

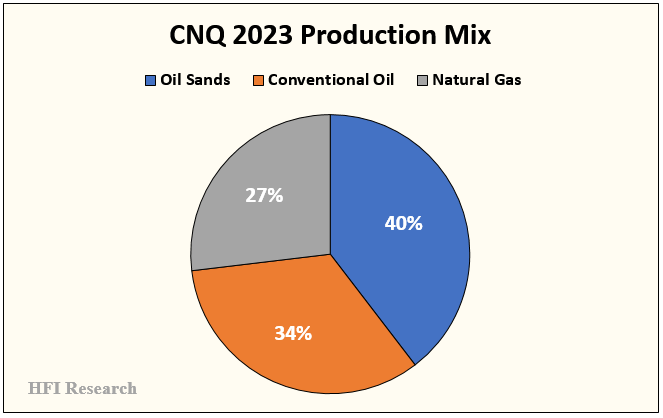

CNQ also is more diversified than the other oil sands operators, as shown in the chart below. Its larger conventional oil and natural gas assets reduce its cash flow torque to higher oil prices on a relative basis.

CNQ’s conventional oil and natural gas production allows for a more flexible operating model than peers. The company can increase or decrease its conventional production in response to oil and natural gas prices. Meanwhile, its oil sands output will remain steady. CNQ’s oil sands operation has massive scale, reducing operating costs and creating a low-cost base of stable, low-decline oil production.

Due to its overall high quality—particularly its low-cost, low-decline, long-lived production base—CNQ can serve as a core oil-weighted holding in a portfolio. We expect the company to achieve management’s $10 billion net debt target in the first quarter of 2024, at which point it will pivot to paying out 100% of free cash flow in the form of dividends and share repurchases. However, this outcome is already priced into the stock. Still, we expect the value delivered to CNQ shareholders on a per-share basis to continue to grow over time.

Oil Price Sensitivity

CNQ is currently trading at a price that implies a WTI price of US$85 per barrel. The shares have not traded off as much as its peers over recent weeks, while its premium multiple causes them to discount a higher oil price. We consider the shares fairly valued based on our expected 2024 production and cash flow estimates, as well as our expectation that oil should trade at or above the mid-US$80s per barrel WTI over the long term.

If WTI remains below US$80 per barrel, however, CNQ shares have some downside, assuming a constant multiple and flat or lower production.

With CNQ shares trading in the high $80s, we rate them as a Hold. We would not add new funds to the name until the shares fall to the low-$80s to ensure a margin of safety in the purchase price. Current owners should hold onto their shares, however, as we expect the share price to grow over the long term due to value creation, assuming the shares retain their relatively high trading multiple.

The primary risk to CNQ shareholders, aside from a long-term decline in oil prices, stems from capital allocation. We assume a significant portion of the $5 to $6 per share or so that will be available for distribution to shareholders in 2024 at US$80 per barrel WTI will be allocated toward share repurchases. With the shares trading at intrinsic value, repurchases would not add to intrinsic value per share. They would have to decline materially in order for repurchases to be the obvious best means of distributing capital. We believe CNQ should instead distribute excess capital to shareholders by increasing its base dividend or paying substantial special dividends.

CNQ could also acquire a large gassy E&P, which could be a risk. The company’s operations already benefit from internally produced low-cost natural gas that gets consumed by its thermal oil sands projects, so additional natural gas production would be sold into the market. If North American natural gas production fails to respond to prices—as is now the case—causing prices to remain low, a gassier CNQ could present downside risk for shareholders, depending on the price paid for the gassy asset and the company’s natural gas production plans.

Conclusion

CNQ is the ultimate conservative alternative among Canadian E&Ps. We expect its shares to continue to trade at a premium multiple, and we expect management to continue to build intrinsic value per share. If oil prices increase considerably, the shares could post solid gains from their current level.

However, its shares are fairly valued, so we rate them a Hold. We favor MEG Energy, Suncor, and Cenovus among oil sands operators for their currently lower trading multiples, the potential for their multiples to increase, their steadily improving operations, and the greater benefits to their shareholders from increased free cash flow distribution, which is set to occur for all three. Investors allocating new funds will be better served amid sustained higher oil prices in these oil sands alternatives to CNQ, all of which we rate as a Buy.

Analyst's Disclosure: I/we have a beneficial long position in the shares of CVE, MEG, SU, CNQ either through stock ownership, options, or other derivatives.