(Public) Canadian Natural Resources - Always Go With The Best

By: Jon Costello

Energy stocks are seeing some of the greatest selling pressure since 2020. Even the highest quality names are plunging in sync with the dregs of the industry when fear spikes and “correlations go to one.”

Due to all the unknowns facing investors over the next few quarters—which include the prospects for a continued stock market meltdown and a global recession—investors should favor quality names that are certain to survive. Once macro conditions stabilize and the market once again distinguishes between high and low quality, these names will rally hard.

And in the event that adverse scenarios don't come to pass, high-quality names will do very well in a more mundane macro environment.

Among high quality, investors should also stick with larger cap stocks, as they’re less at risk of a “take-under” if macro conditions deteriorate further. A take-under is the situation when an investor buys a stock that ends up being acquired at a lower price, forcing a permanent capital loss.

One of The Highest Quality E&Ps

Among global E&Ps, we’re hard-pressed to find a higher quality large name than Canadian Natural Resources (CNQ) (CNQ:CA).

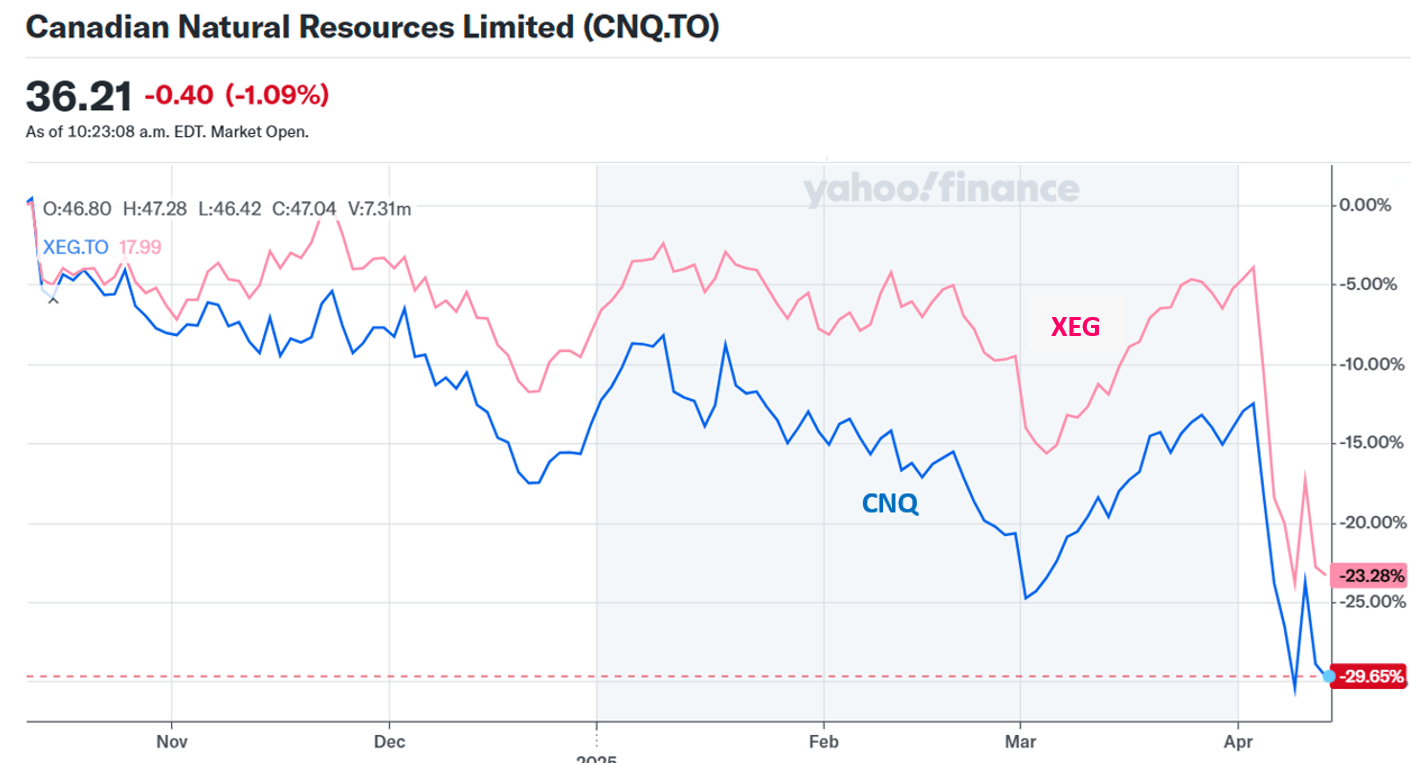

Even before this recent selloff, Canadian Natural Resources CNQ’s stock was under pressure relative to its peer group. Its shares began to underperform late last year. The underperformance grew larger throughout 2025, as shown below.

Source: Yahoo! Finance, April 12, 2025.

CNQ benefits from having one of the lowest free cash flow breakeven costs per barrel in the North American oil patch. We estimate its free cash flow remains positive at maintenance capex levels down to US$40 per barrel WTI. It will therefore survive any conceivable downturn and possibly emerge in stronger shape.

CNQ’s Headwinds

Three factors have weighed on CNQ shares in recent months outside the broader energy sector negativity and general market panic.

First, some investors are concerned that CNQ has grown too large to sustain the outsized organic production growth it has achieved since its founding in 1989. Second, the company is vulnerable to U.S. tariffs. Third, free cash flow distributions to shareholders were recently adjusted lower, from 100% to 60%. These factors are the reason for the stock’s underperformance relative to its sector.

1. CNQ’s Large Size

There is merit in the first concern, namely, that CNQ has grown too big to sustain outsized growth. After all, the company’s market cap stands at $77 billion against a backdrop of the approximately $200 billion market cap of Canadian E&Ps. Nevertheless, important considerations make this concern overblown.

Firstly, CNQ’s long reserve life ensures it can grow organically over at least the next five-to-ten-year period. The company’s proved reserve life extends some 26 years, far longer than any of the oil majors’ E&P operations.

Moreover, CNQ’s long-term growth target is not particularly heroic. The company intends to grow production in the low-single-digits percentage range, which should be manageable over at least the next few years. Its targeted growth rate is only slightly lower than those of its smaller Canadian E&P peers, such as Whitecap/Veren (WCP:CA), Strathcona Resources (SCR:CA), Cenovus Energy (CVE:CA), and MEG Energy (MEG:CA).

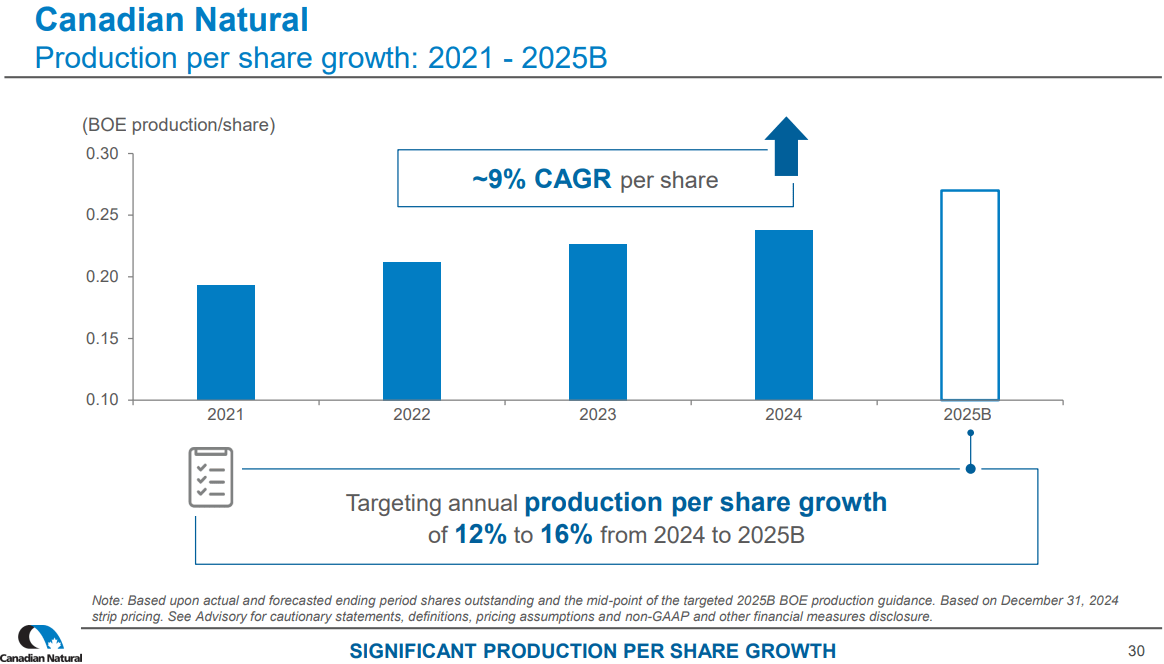

Secondly, shareholders should consider growth from a per-share perspective. CNQ’s low free cash flow breakeven and high return on capital ensures accretive share repurchases as the cycle turns down and its share price falls. Repurchases will continue the company’s longstanding trend of increasing production, reserves, and cash flow over time on a per-share basis. The chart below illustrates the steady upward trajectory of production per share.

Source: CNQ April 2025 Investor Presentation.

Thirdly, acquisitions still provide a potential avenue for growth. Whether growth comes from existing resources or an accretive acquisition shouldn’t matter under a top-notch management team like CNQ’s.

CNQ’s management and its top-tier assets lock in a higher-than-average return on capital, potentially for decades. Consequently, its shares trade at a higher multiple than peers. As a result, it can use its shares to acquire low-priced assets and companies on an accretive basis for shareholders.

Much of CNQ’s growth has come through acquisitions during downcycles. No doubt the company’s leadership will be on the hunt for high-quality assets that complement the company’s existing asset base if the current downturn persists.

The company’s most recent acquisitions illustrate how it creates value through acquisitions, even in the good times.

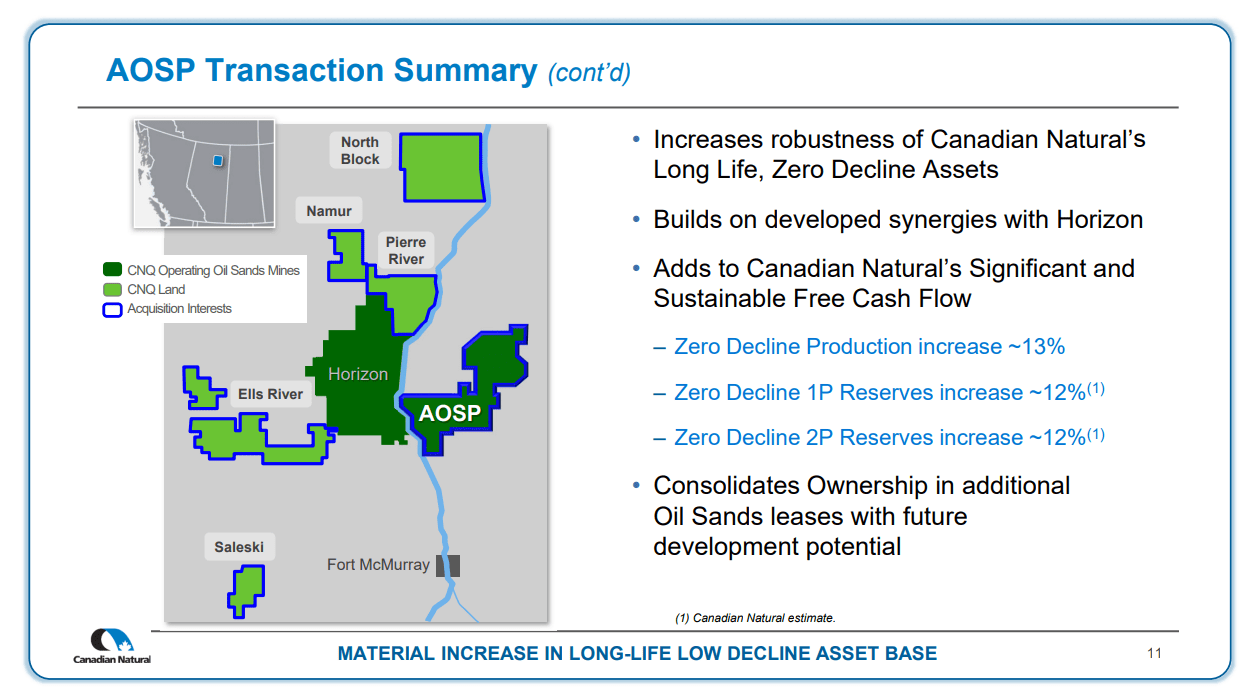

CNQ closed its US$6.5 billion acquisition of Chevron’s (CVX) Athabasca Oil Sands Project (AOSP) in December 2024. The deal added zero-decline SCO mining reserves and operating optionality to CNQ’s high-quality and diverse oil reserve base. The assets are in close proximity to CNQ’s existing Athabasca assets.

Source: CNQ AOSP Acquisition Presentation, December 2024.

It also brought Chevron’s 70% interest in Duvernay acreage producing 60,000 boe/d.

Then in January, CNQ swapped its 10% interest in the Scotford synthetic oil upgrader and certain carbon capture facilities for Shell’s (SHEL) 10% interest in the AOSP.

The December and January AOSP deals increased CNQ’s working interest in the project from 70% to 100%, adding 31,000 bbl/d of synthetic crude oil production at a low cost. CNQ will still operate and own an 80% interest in the Scotford upgrader. We wouldn’t be surprised to see the company make additional deals to increase its stake in the upgrader.

These moves illustrate the long-term strategic brilliance of CNQ’s management when it comes to acquisitions. The company has proven its ability to build shareholder value by consistently buying assets from motivated sellers. Its acquisitions have increased the quality and volumes of its oil production and reserves on the cheap. We would expect other such deals to emerge if the current downturn remains in place for another few months.

2. Vulnerable to Tariffs

The second investor concern about CNQ is its vulnerability to U.S. tariffs. This is an inescapable reality, but we don’t expect U.S. tariffs on Canadian oil production to be in place for long. We therefore view the current concerns as a buying opportunity for investors with a time horizon of more than a year. Once the tariff threat is gone, CNQ shares are likely to bounce back to the mid-$40s in short order.

3. Reduction in Shareholder Capital Returns

CNQ used debt to fund its $6.5 billion AOSP acquisition. In order to reduce the debt taken on to fund the deal, it changed its free cash flow distribution policy from paying out 100% of free cash flow after dividends to paying out 60% of free cash flow after dividends. Investors were miffed about the sudden and unexpected change to the long-anticipated 100% payout.

We view this as another temporary situation that long-term investors can use to their advantage.

CNQ is allocating 40% of its free cash flow to pay down debt. Even at US$60 per barrel WTI, it will pay down this debt rapidly over the next few quarters. Of course, there is a risk that it will take on additional debt to fund another acquisition during this downturn, but we suspect that any acquisition will be highly accretive to intrinsic value. As such, it is likely to offset the negative impact of reduced variable dividends and/or share repurchases.

Operating Performance Remains Stellar

CNQ continued its outstanding operational execution yet again in the fourth quarter.

Adjusted funds from operations were 3% higher year-over-year. Production hit a record, while capex came in 6% lower than analyst expectations.

The performance allowed the company to return $1.7 billion to shareholders in dividends and share repurchases. CNQ also raised its common dividend by 4% to an annualized rate of $2.35 per share. On the current share price of $36, the dividend yields 6.5%, two full percentage points higher than its average yield throughout 2025.

CNQ Shares are Cheap

CNQ shares are trading at a rarely seen discount. For years, large institutions owned CNQ stock as a conservative way to gain long-term exposure to oil. We suspect that many of these funds are being forced to raise cash for various reasons by selling their most liquid positions, such as CNQ. The indiscriminate selling is causing most high-quality stocks to trade down in sync with their smaller peers. High-quality E&Ps have sold off worse than most other large caps outside the energy sector.

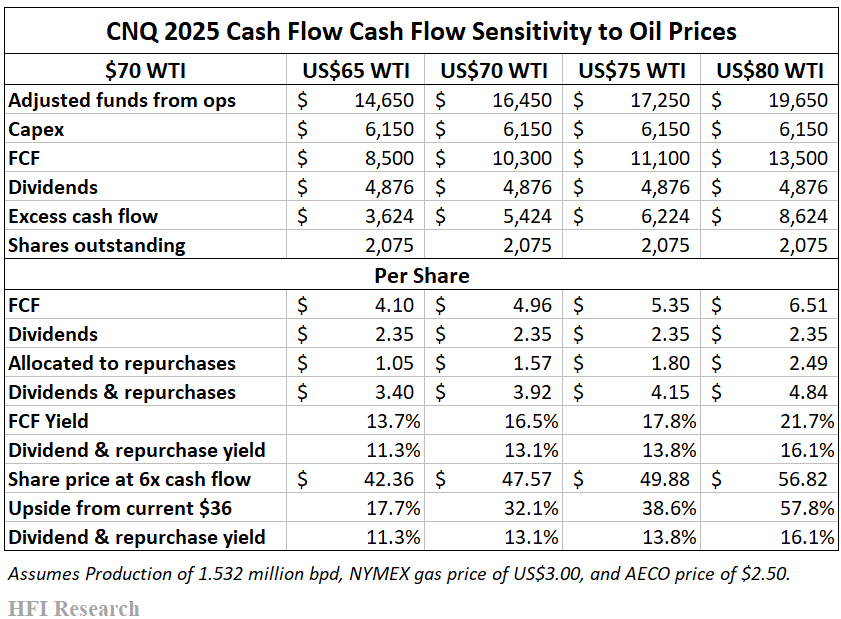

This selloff has brought the CNQ share price down to juicy territory for conservative investors who seek income and long-term capital appreciation. The following table illustrates the company’s free cash flow potential at different oil prices and the upside potential in its shares.

We’re confident that WTI will see US$80 per barrel once again. At that level, the nearly 60% upside potential in CNQ shares is very attractive for a large-cap stock. And the return estimates exclude dividends. CNQ offers the additional benefit of being conservative enough to be held in size at current prices for investors with a multi-year time horizon.

Barring a global depression, we estimate that WTI under US$70 per barrel isn’t sustainable for more than a year. As this downturn runs its course and oil prices recover, the shares are all but certain to respond by trading higher in response to CNQ’s surging cash flow.

In the meantime, investors can benefit from CNQ’s 6.5% dividend, which will be sustained in any realistic scenario. In the brutal conditions of 2020, the company kept its dividend intact. We believe it will do the same in 2025.

Conclusion

Investors won’t find many better alternatives among large-cap E&Ps than CNQ. The shares are as close to a set-it-and-forget-it proposition as an investor will find in the sector. At the current price of $36 per share, investors interested in both capital appreciation and income should consider making a long-term investment in these shares.

Analyst's Disclosure: Jon Costello has a beneficial long position in the shares of CVE, SCR.TO, MEG.TO either through stock ownership, options, or other derivatives.