(Public) The Negativity Toward Cenovus Energy Is Overdone

Cenovus Energy's (CVE) stock has lagged behind its large oil sands peers—badly. Since the beginning of 2023, it's gained 6.97%, versus 36.92% and 27.20% for Canadian Natural Resources (CNQ) and Suncor Energy (SU), respectively.

CVE fell out of favor in 2022 after management miscommunicated the timing of the company’s pivot to returning 100% of free cash flow to shareholders. Around the same time, another headwind to the shares’ performance emerged when CVE’s U.S. downstream segment suffered a series of outages and delayed refinery restarts. The U.S. downstream segment's sub-par performance reduced refinery throughput, which crimped companywide margins and created a drag on CVE’s financial results for multiple quarters.

However, CVE is on the verge of both operating and financial improvement. Its downstream segment is fully operational and is experiencing a multi-quarter throughput ramp. Upstream, CVE’s heavy oil production is poised to grow, while its West White Rose project will accelerate production growth over the coming years. In total, management expects 150,000 boe/d of production growth over the next five years, equivalent to 19% of the company’s current production of approximately 800,000 boe/d.

In addition to dour investor sentiment, temporary market factors are also offsetting the impact of CVE's positive company-specific developments. Weakening oil prices and refining margins will pressure second-quarter results, so investors are waiting until the smoke clears before purchasing shares.

Investors who can look beyond these temporary negatives should consider buying CVE shares. Today’s share price provides an outstanding entry point for either a short-term or longer-term holding.

Reasons for Optimism

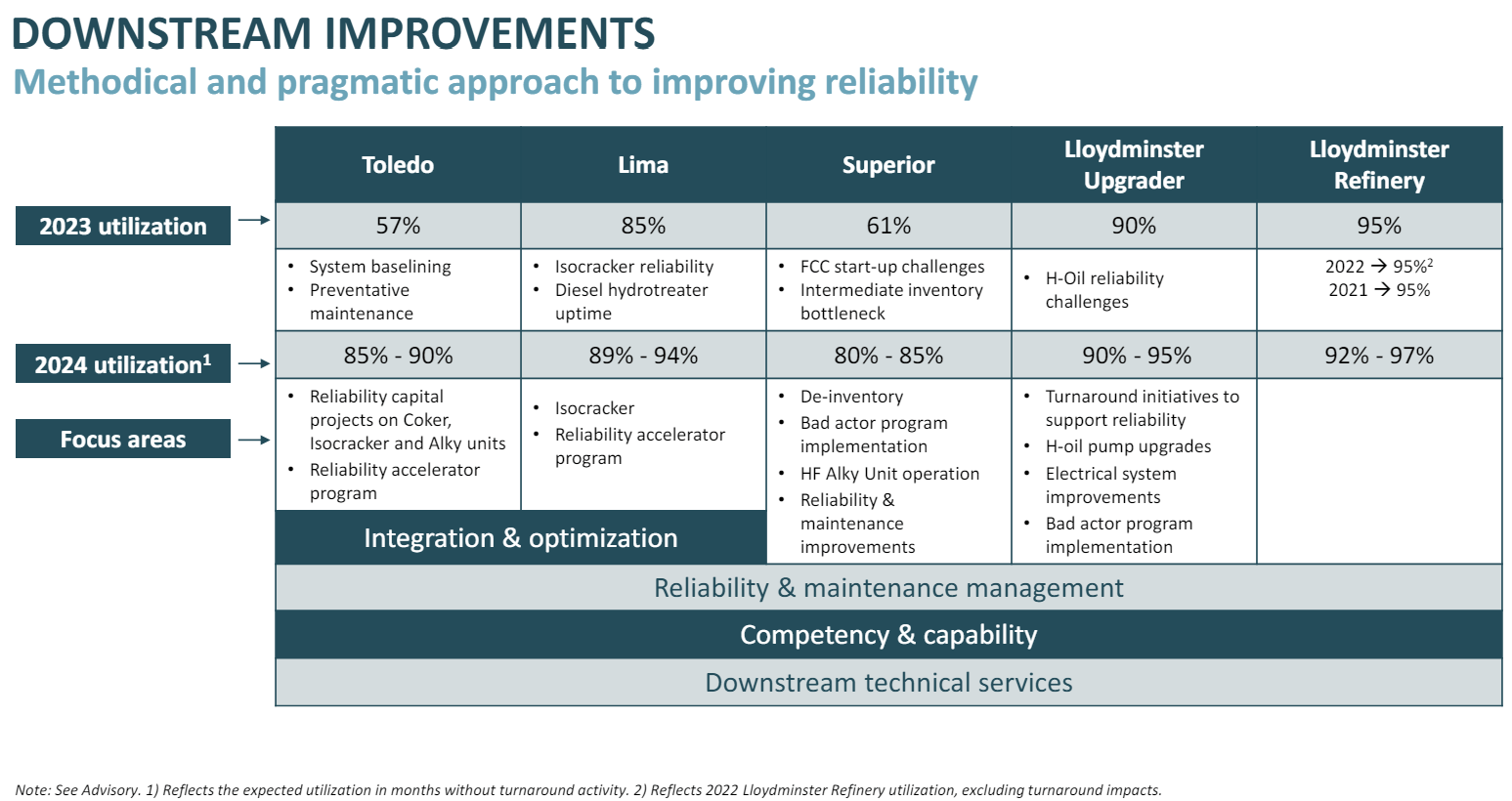

Our optimism toward CVE's prospects stems from the fact that the company hasn’t yet begun to demonstrate the full potential of its integrated value chain. U.S. refinery throughput has increased quarter after quarter, most recently reaching a greatly improved 87% in the first quarter of this year after having averaged 75% in 2023. Despite the improvement, U.S. refinery throughput remains below its full potential. CVE’s Canadian downstream segment routinely operates at throughput rates in excess of 90%, hitting 94% in the first quarter. The entire downstream segment’s per-unit economics will improve further once the performance of CVE's U.S. refineries can match that of its Canadian refineries.

The chart below shows how continued improvements in the U.S. downstream segment throughout 2024 and beyond will provide a significant boost to CVE’s free cash flow. It also illustrates that increasing per-barrel refining margins can drive large increases in the segment’s total margin contribution. For context, weakness in the U.S. downstream segment drove CVE’s total downstream margin to a disappointing C$477 million in 2023.

Source: CVE Investor Presentation, May 2024.

Operating improvements that drive financial improvements will greatly move the needle for the company’s free cash flow. Management points to the following downstream operating improvements in 2024:

Source: CVE Investor Presentation, May 2024.

We estimate that a normal downstream segment margin contribution in excess of $1 billion will allow CVE to consistently generate a return on capital employed of more than 20% with WTI above $80 per barrel. Such a high return on capital could cause an increase in CVE's trading multiple.

Near-Term Positives

CVE is on the cusp of reaching its $4 billion net debt target. Once the target is hit, it will pay out 100% of free cash flow to shareholders through share repurchases and dividends. The company’s growing free cash flow generated amid higher oil prices can then flow directly to shareholders.

We expect CVE’s net debt target to serve as a catalyst for improved investor sentiment toward the name. Improved sentiment will eventually bring a higher share price. We already own CVE shares in our income portfolio, but we’re considering adding CVE to our trading portfolio, as well, to capture near-term appreciation. We’d note that Canadian Natural Resources shares underwent a re-rating to a higher trading multiple when the company transitioned to paying out 100% of free cash flow. CVE shares could undergo a similar re-rating relative to their own historical trading multiple.

The bullish macro setup for oil prices is another near-term positive for CVE shares. We expect increasing oil demand during the summer driving season coupled with flat supply to drive inventories lower and prices higher. When CVE’s enhanced capital allocation policy meets higher oil prices, its shares could play catch-up with the performance of CNQ and SU.

We’re also gratified by CEO Jon McKenzie’s confidence in CVE shares. So far in 2024, McKenzie has bought 225,000 shares for C$5.67 million at an average cost of C$25.20 per share.

The Longer-Term Outlook

Over the next few years, we anticipate an increasingly bullish macro backdrop for the oil market. Global oil demand will continue to grow, while the world’s primary engine of production growth—U.S. shale—will mature. Shale will reach the point where its production will be at risk of declining if oil prices fail to trade at levels high enough to incentivize a minimum number of drilling rigs. At the same time, without higher prices, production growth outside of shale and OPEC+ will remain subdued.

As the focus in the oil market turns to supply, investors will begin to appreciate the risk of owning E&Ps with short reserve lives. They will increasingly seek out those with long reserve lives that generate significant free cash flow. We expect CVE to be a top pick.

WTI sustained above $80 per barrel will be particularly positive for CVE and its shareholders. As its cash flow grows, its dividends will increase while its declining share count will result in growing free cash flow and dividends per share.

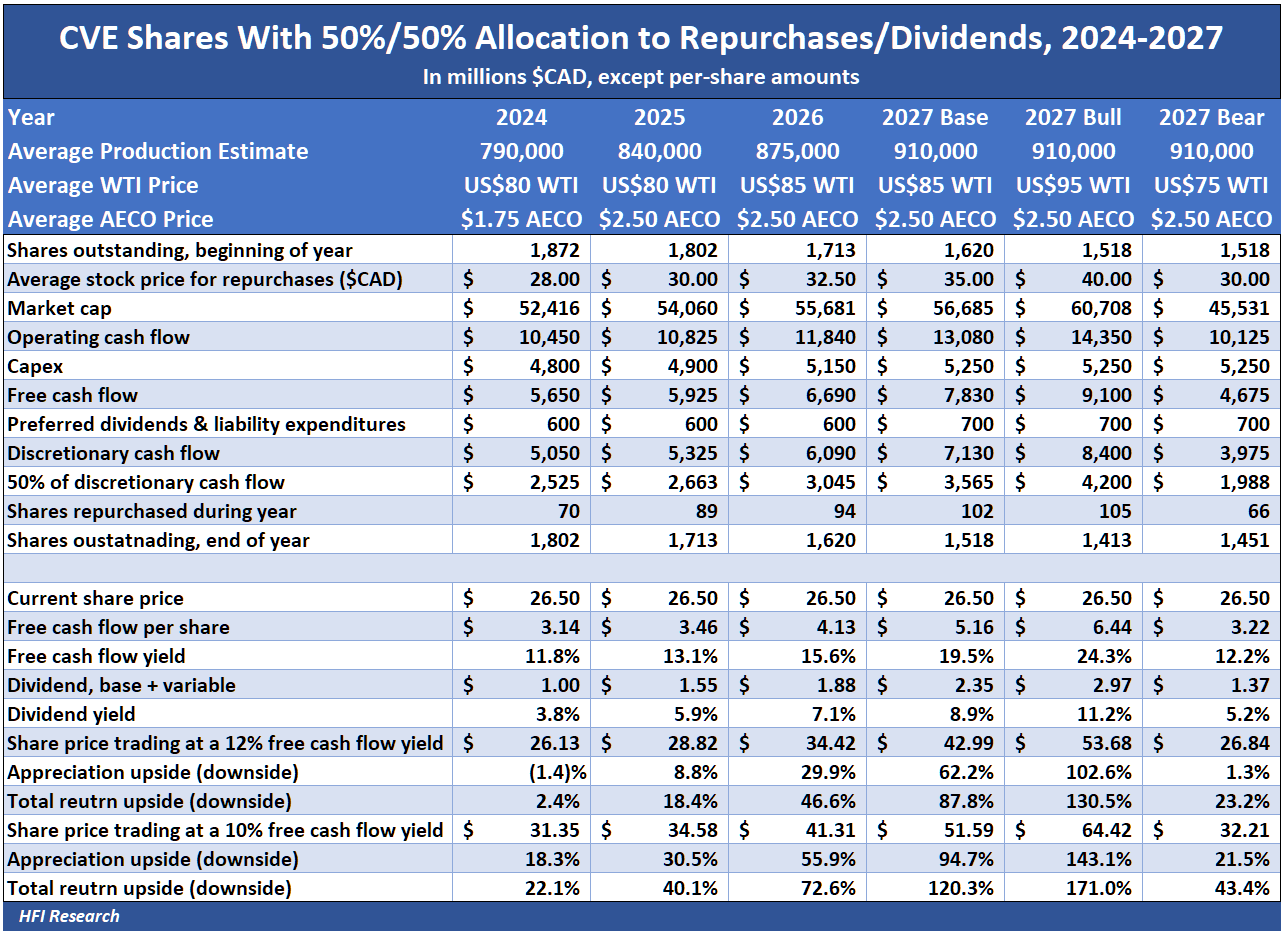

The following table shows our free cash flow and share price estimates for CVE through 2027. It assumes free cash flow is allocated 50% to dividends and 50% to share repurchases. Production growth and our expectation of higher oil prices drive the shares' return prospects significantly higher.

Like all E&Ps, CVE shares will remain at risk from a bout of lower oil prices. Nevertheless, their long-term return prospects are overwhelmingly favorable from the current stock price of C$26.50 and US$19.25. We estimate the shares’ expected total return through 2027 is 80.5%, assuming they trade at a 12% free cash flow yield. If they trade at a 10% free cash flow yield, our expected total return increases to 111.6%.

In terms of downside, WTI at $75 per barrel WTI in 2027 lowers total return potential to 23.2% through 2027, pointing to significant long-term downside protection.

Conclusion

CVE is in the doghouse, but improvements are underway. As they become evident to the market, sentiment will improve, and CVE shares will regain their favor. The combination of a discounted stock, near-term catalysts, and attractive long-term economics make the shares among the most attractive large-cap oil E&Ps in today’s stock market.

Analyst's Disclosure: I/we have a beneficial long position in the shares of SU either through stock ownership, options, or other derivatives.