By: Jon Costello

The chaotic trading in the energy sector has been a sight to behold. The investing public has left the sector for dead, and even the most attractive names are now selling at extremely attractive levels.

But babies are being thrown out with the bathwater in all parts of the sector. For investors brave enough to take the plunge and buy, a few names stand out at current prices.

Exxon Mobil (XOM)

XOM has sold off in response to its guidance last week for higher-than-expected capex over the next few years. The selloff has caused XOM to enter an attractive buy zone. At current prices, XOM is our favorite stock among the global oil and gas majors.

Investors were miffed after the company announced plans to spend between $28 and $33 billion annually on capex through 2030, above consensus expectations of $26 billion. Next year’s capex also came in high, at $27 billion versus expectations of $26 billion. The $25 billion in base capex was in line with expectations. Market concerns centered on the growth component, a large portion of which will fund production growth in the Permian.

The company has big plans to boost oil recoveries in the Permian. Most revolve around new technologies in a wide variety of areas. We don’t have enough engineering expertise to opine on the prospects for XOM’s new technology to increase oil recoveries. That said, some of its recently-developed technology looks promising, like its new coke-based proppant.

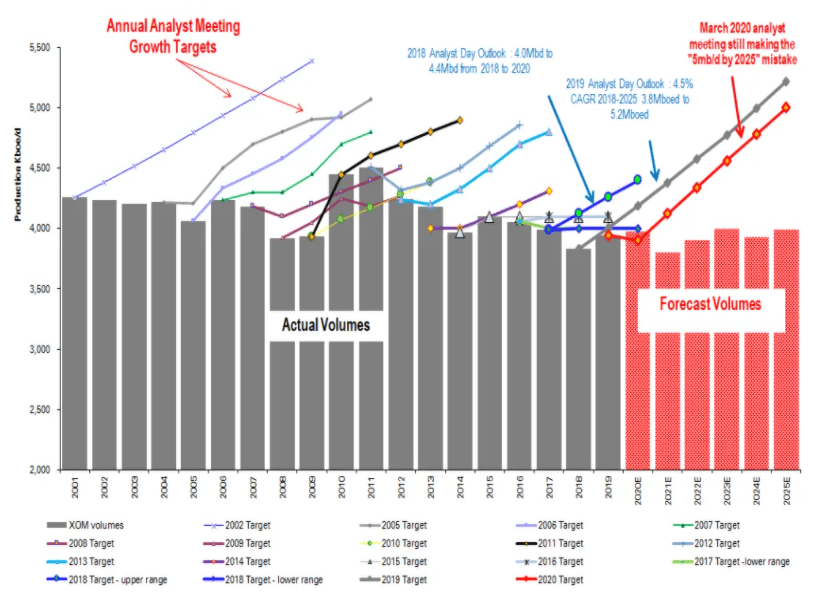

But if history is any guide, XOM will set high growth targets and then fail to meet them by a mile. The chart below, made by Paul Sankey back in 2020, illustrates the historical pattern.

Source: Paul Sankey, X, Dec. 1, 2020.

To be sure, history could repeat, and XOM could disappoint. But we’re not so pessimistic this time around. Management has navigated this aircraft carrier of a company superbly, focusing its upstream oil operations on highly prospective projects in Guyana and the Permian. We don’t believe their guidance is mere bluster. More than a little production growth is likely; the only question is how much Permian production consists of crude versus lower-value NGLs and natural gas.

If the company succeeds at increasing its Permian recoveries, it will wring significant additional crude oil volumes out of future production. With more than 15 years of high-quality drilling inventory, shareholders will benefit from sustained higher cash flow.

Permian growth won’t begin until 2026. For 2025, XOM is guiding for 1.5 million boe/d of Permian production, down from this year’s 1.6 million boe/d.

Beginning in late 2025 and picking up stream in 2026, XOM’s higher capex will drive production increases in the Permian, Guyana, and its LNG operation. Altogether, its upstream assets are expected to drive 1.2 million boe/d of incremental production by 2030, nearly 30% above today’s 4.2 million boe/d. The company is also guiding to more than $9 billion in upstream earnings potential at $65 per barrel Brent, equivalent to more than $2.00 per share at the current share count. At today's 13x P/E, that's an additional $26 on the share price, which today stands at $106. Of course, the numbers grow much larger if oil prices are sustained at higher levels, as we expect.

In most cases, investors are right to pan higher capex guidance. After years of poor investment returns, most prefer that energy companies keep capex flat and return excess capital to shareholders. We believe that view is misguided in XOM's case. By the 2027-2030 timeframe, we expect the world to need additional oil. We’re pleased that some will be sourced in the U.S. As global supply grows increasingly constrained over this period while XOM’s production ramps higher, we expect the company to benefit from both increasing production and higher oil prices. By then, natural gas prices may also be sustained at higher levels, delivering an additional boost to XOM’s bottom line. The company has been outstanding at capital allocation—the best among its major peers—so shareholders can be confident that higher earnings will be distributed as dividends and share repurchases.

XOM shares aren’t the cheapest in the energy space. But the company’s operational scale and diversification make its shares extremely safe. Moreover, XOM’s future is clear compared to its peers, making its stock attractive on a relative basis. The shares’ safe 3.6% yield is appetizing, with embedded inflation protection from its commodity exposure.

Veren (VRN)

I’ve been harping on this name since early November. The shares can’t get a break, trading down day after day after day. Check out the chart of this falling knife since May:

Count me among the bloodied knife catchers. I bought shares for our HFI Research Energy Income portfolio at $5.08 and again at $4.66.

Despite the horrible price action, I’m optimistic about this name. Here is a recap of some of the salient facts.

Management screwed up by completing a large batch of 12 wells with plug ’n perf instead of single-point entry. Bad on them.

Nearby wells, even offsetting wells, show results on par with previously drilled wells, indicating the problem is not one of geology but completion technique and risk management.

A chastened management team—which this one clearly is—is far less likely to repeat the same screw-up. The pressure is on to improve well results, and we believe management can execute.

VRN is one of the largest acreage holders in the Montney. Its acreage is more liquids-rich than its Montney peers. Despite the recent poor well results, VRN has drilled some of the best wells in the play.

Duvernay production will drive most of VRN’s growth.

VRN’s five-year plan has been delayed, but still holds the prospect for growth to levels of more than 245,000 boe/d over the next five years from the 191,000 boe/d guided for 2025.

The shares are trading at an EV/DACF of less than three times at $70 per barrel WTI. At $80 per barrel, they’re closer to 2.5 times, reflecting the shares’ bargain pricing.

Continued debt reduction will increase value for shareholders. Share buybacks made at current price levels will be highly accretive.

Assuming well results improve, VRN’s attractive return on capital amid anything but unsustainably low oil prices will drive investor sentiment toward the name higher.

The stock price will rebound with investor sentiment.

Abysmal sentiment has caused investors to overlook these realities. As a result, VRN shares have closely tracked Baytex Energy (BTE), but VRN is very different than BTE. So much so, in fact, that a comparison is silly.

The high correlation between the two underscores investors' misunderstanding of VRN and its long-term prospects.

The heavy trading volume in VRN's shares suggests significant tax loss selling. This selling pressure will abate at year-end. Over time, I expect investors to become more interested in the name and to bid its shares back to levels above $6 per share.

VRN shares offer the combination of a safe and attractive dividend yield of 7% and more than 100% appreciation potential over the next three years. Appreciation potential increases thereafter as the company’s scheduled 2027 production ramp bears fruit in the form of increased cash flow, dividends, and share repurchases.

Pembina Pipeline (PBA)

For the income crowd, Pembina has sold off to attractive levels. This company offers a simple story. Its expertise in building and operating gathering and processing infrastructure for oil and gas exposes it to Canadian oil and natural production growth without commodity price risk.

The shares now yield 5.4%, which is attractive in light of the company’s long-term dividend growth and capital appreciation prospects.

Longtime readers know we seek protection through growth in our income equity investments. PBA offers a case in point.

Whereas many of PBA’s U.S. peers face growth constraints due to a significant infrastructure buildout over recent years and soon-to-plateau U.S. oil production, Canada will continue to grow, and PBA will continue to expand in the Western Canadian Sedimentary Basin.

Its continued growth will drive its cash flow and dividend payout higher. Its excellent capital allocation is likely to ensure that investments are well made and excess cash flow is returned to shareholders.

PBA offers investors the kind of package that has driven midstream stocks relentlessly higher since 2020: volume growth that translates into cash flow growth, lower debt, and higher capital distributions to shareholders. PBA shares still have a long runway to benefit.

Conclusion

For investors with strong stomachs, this is an outstanding time to add to well-positioned energy stocks like XOM, VRN, and PBA. I have no special insight into how their stocks will perform over the coming months, but I’m highly confident that investors will be pleased with their returns over the next two years and beyond. This is the time to get long.

Analyst's Disclosure: Jon Costello has a beneficial long position in the shares of VRN either through stock ownership, options, or other derivatives.

More on XOM:

- 95% of projects return a 10% IRR at $35 oil.

- 2027 FCF expected to be $62bn at $65 oil.

- All CapEx going on projects with a 40% IRR at $65 oil.

Take. My. Money