(Public) What Trump's Victory Means For Energy Stocks

By: Jon Costello

Donald Trump’s victory has far-reaching ramifications for the oil and natural gas markets. All in all, we believe they’re net bullish. Wilson covers them in detail here.

Trump’s victory has ramifications on a micro level as well, for oil and gas companies and their stocks. We'll cover them in this article.

A Boost to Investor Sentiment

Right off the bat, we expect investor sentiment toward oil and gas stock to improve now that oil and gas projects are less likely to be hobbled by red tape. I expect attempts to phase out oil and gas to fall out of favor as efforts to reduce demand continue to fail. As a result, oil and gas asset values can avoid being held down by perceived “stranded asset” risk.

The sentiment boost can be seen in today's 5.2% rally in the E&P-weighted XOP ETF (XOP) and 3.8% rally in the broad-based energy sector XLE ETF (XLE). Both occurred in the face of lower oil prices.

Higher asset values and lower perceived risk to long-term demand will incentivize E&Ps to pursue new long-cycle projects. These are essential for sustaining enough production to meet growing demand over the long term. I expect the oil and gas majors—particularly the European players like BP (BP) and Shell (SHEL)—to regain some of the mojo they lost pursuing renewables over the past few years.

Energy Policy Will Change for the Better

The Trump administration’s biggest impact on energy stocks will come from its approach to energy policy and regulations. This is where the big changes from the Biden administration will occur.

First and foremost, the Biden administration’s sprawling energy regulatory apparatus will be reined in.

Under Biden, regulators widened the scope of their domain to an unprecedented degree.

In the upstream space, the Biden administration raised oil and gas royalty rates on federal lands and suspended new oil and gas lease sales on federal lands and waters. Fortunately, these regulations did little to hold back shale oil production, which grew to all-time highs under Biden’s watch.

The Biden administration’s most harmful regulations came through a highly activist EPA and a FERC that was given an expanded mandate to regulate energy project emissions. The regulatory patchwork that emerged created a playground for lawyers who sought to halt major oil and gas projects up and down the oil and gas value chain.

Lawfare campaigns caused the cancellation of major midstream projects, including the Northern Access Pipeline, Atlantic Coast Pipeline, and Constitution Pipeline. The Mountain Valley Pipeline and the Dakota Access Pipeline narrowly escaped becoming casualties.

Trump will scale back the Biden administration's regulatory apparatus through executive orders, cabinet appointments, and political influence with a Republican Congress. Less regulation would lead to a more vibrant domestic energy sector. It will lower energy costs for consumers and ensure the security of supply.

No Appreciable Impact on U.S. E&Ps

Biden administration regulations didn’t impact drilling activity in the shale patch, so U.S. oil production reached record highs during its tenure. Under Trump, we expect the upward trajectory of U.S. production to continue at a more gradual rate in the low-single-digits percent annually.

Many investors are concerned that Trump’s “drill baby drill” platform will bring forth a torrent of shale oil, sending oil prices lower and causing Saudi Arabia to launch a market share war. We don’t share these concerns at all.

U.S. E&Ps are constrained by geological and economic challenges. These render any political imperative to boost production dead on arrival. None of our E&P valuations have changed due to Trump’s victory. We expect most public E&Ps to operate in maintenance mode to extend Tier 1 inventory and maximize reserve life. The sector’s consolidation will continue.

The Biggest Impact Will be on U.S. Midstream

Trump’s impact on midstream will be direct and impactful.

Midstream Deregulation

If Trump can scale back the Biden administration’s regulations, midstream oil and gas activity could accelerate across the country. For the first time in many years, midstream operators will be able to plan and budget with the expectation that large-scale projects will enter service on time and on budget.

Targa Resources (TRGP) will be able to execute its newly announced growth projects at low risk. Energy Transfer (ET) will obtain the necessary permits for its Lake Charles LNG export facility, which had been held up by the Department of Energy. EQT (EQT) will be able to complete the MVP Southgate project, which was shelved by Equitrans Midstream due to completion risk.

Keystone XL

Keystone XL will be an exception. I don’t expect the project to restart as some industry watchers do. The project has already been terminated and dismantled at a cost of $1.8 billion to its developer, TC Energy (TRP).

Moreover, there are enough Biden-appointed judges who presumably oppose the project to obstruct its completion. If TRP intends to pursue the project, it will have to begin the process right away to make it through all the legal challenges and avoid another potential cancellation in 2028.

A restart will require a long process of preparation that the company probably isn’t willing to pursue, particularly in light of the disaster that occurred the last time. We own shares in TRP and have seen no indication that it is interested in the project.

LNG Development

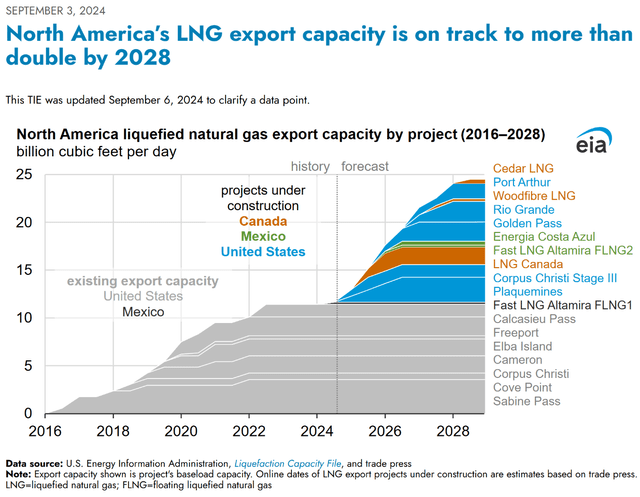

Trump will eliminate Biden’s executive order mandating a “pause” on LNG export development. This will clear the way for the North American LNG buildout to continue. The facilities already scheduled to come online through 2029 aren’t likely to face further delays.

Source: EIA, Sept. 3, 2024.

An obvious beneficiary is Cheniere Energy (LNG), a longtime holding in our HFIR Energy Income Portfolio. Cheniere will now be able to complete its Sabine Pass and Corpus Christi expansion projects over the next few years.

Knock-On Effects of LNG Exports

With an improved outlook for LNG facility construction, U.S. and Canadian natural gas-weighted E&Ps can look forward to the day that demand for their product undergoes a step change higher. I expect higher natural gas prices, at least for a few quarters, which will facilitate deleveraging and capital distributions to shareholders. EQT (EQT) and Antero Resources (AR) in the U.S. and Tourmaline Oil (TOU:CA), ARC Resources (ARX:CA), Peyto Exploration (PEY:CA), and Spartan Delta (SDE:CA), are our favored ways of playing increased natural gas demand.

TRP, Pembina Pipeline (PBA), Enterprise Products Partners (EPD), and Energy Transfer (ET) are attractively-priced stocks that are poised to benefit from favored positions and massive scale in the midstream space. We’d avoid new buys of our favorite midstream U.S. corporations, Targa Resources (TRGP) and Oneok (OKE), as their stocks are fully valued at the moment.

IRA on the Chopping Block

The incoming Trump administration will target parts of the Inflation Reduction Act (IRA) for cuts. The costs of IRA energy provisions have grown far above their original estimates. Many rules have yet to be finalized, and I expect Trump to cancel those that can be eliminated without legislation. He is also likely to rescind a portion of unspent funds allocated by the IRA.

IRA programs and projects currently underway will be treated differently under Trump. I don’t expect the incoming administration to tamper with these initiatives as much as Trump’s rhetoric suggests.

First off, large-scale changes in many IRA provisions would require legislation. Even a Republican-controlled Congress will struggle to implement significant changes. Major changes to the RINs or Low-Carbon Fuel Standards that are already in place are not likely to pass.

Second, many of the IRA’s beneficiaries have already made large investments in the infrastructure and systems called for by the legislation. A large percentage of these projects are located in Trump-friendly regions in the middle of the country. They support local economies and jobs, and as such, they’re likely to remain in place.

Most of the changes to the IRA will fall to the cabinet members that Trump appoints. Until they’re announced, it will be difficult to see the administration’s approach toward IRA provisions.

The Global Energy Ramifications of Trump’s Victory

Trump’s victory has an underappreciated global dimension, which I expect will influence global energy markets.

Trump is the latest in a wave of conservative political victories that is sweeping through South America, Europe, and now, North America. All these movements are different in their particulars, but they have one thing in common: they represent a backlash against incumbents and their green agendas. The newly elected politicians are turning away from a focus on climate change above all else and are instead prioritizing energy access, affordability, and security.

Impact on Canada E&Ps

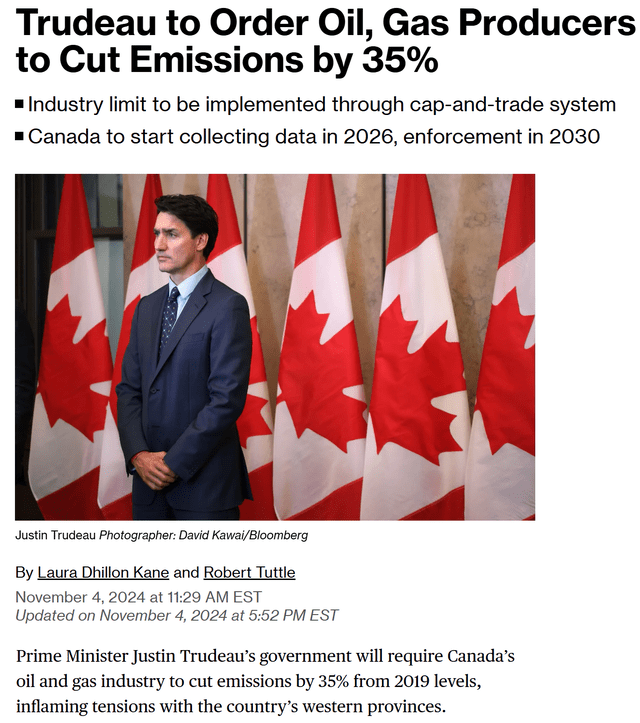

After Trump’s win, I expect that Justin Trudeau, the prime minister of Canada, will be one of the next incumbents voted out of office. Trudeau’s administration has launched a program aimed at reducing Canada’s carbon emissions by 40% to 45% below 2005 levels by 2030. If fully enacted, the measures would significantly raise taxes and could cause the curtailment of Canadian oil volumes.

On Monday, the Trudeau administration took direct aim at the Canadian oil and gas industry by proposing a cap-and-trade system that threatens to reduce Canada’s oil production growth prospects.

Source: Bloomberg, Nov. 4, 2024.

The momentum that Trump’s victory delivered to the global conservative wave makes it more likely that Trudeau will lose his reelection bid in October.

This is a clear positive for our favorite E&Ps, which reside in Canada. It significantly reduces the risk that these companies will face increased taxes and long-term production limits. Healthy Canadian oil and natural gas production will also benefit U.S. midstream and export volumes for many years.

It increasingly looks like Trudeau will be unseated by Pierre Poilievre, an avowed advocate for Canadian energy. Shares of MEG Energy (MEG:CA), Cenovus Energy (CVE), Suncor Energy (SU), and Strathcona Resources (SCR:CA) are all attractive alternatives that will prosper under Poilievre. We’re more confident in our long-term E&P cash flow estimates, knowing that the companies are not likely to face harsh regulations.

Impact on International E&Ps

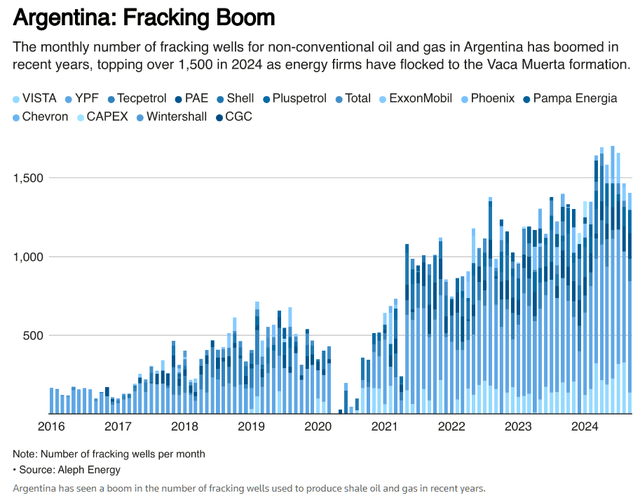

The rightward political shift sweeping the globe will give global E&Ps greater leeway to grow production. Attractive emerging prospects include the Vaca Muerta shale formation in Argentina. Among the E&P beneficiaries are oil majors such as ExxonMobil (XOM), Chevron (CVX), and Total (TTE). Other smaller international E&Ps also stand to benefit, some of which are listed in the chart below.

Source: Reuters, Oct. 23, 2024.

From a macro perspective, additional supply will be a bearish variable for the oil market over the next few years. However, if deregulation occurs on a global scale, it will deliver a boost to economic growth that will more than offset its impact on supply.

Impact on Oilfield Services

Offshore production—the next frontier for marginal supply—will receive more attention and more capital. Offshore service providers such as Transocean (RIG), Valaris (VAL), and Tidewater (TDW) will see increased demand for their rigs and ships. All three had fallen to low levels relative to value over the past few months and rallied hard today in a mixed tape for energy names.

Trump’s Victory and Crude Oil Futures Pricing

I’ll sneak in one final comment on the sensitive topic of the whacky crude oil price behavior that has occurred since August. With the Biden administration on its way out, I expect far fewer incidents in which oil futures get slammed lower in response to bullish news. Hopefully, the recurring Friday selloffs will also be a thing of the past.

The recent price behavior in the oil futures market has caused fundamental-based traders to exit the market. The market is now dominated by algos that employ momentum strategies that carry prices too far for no apparent reason. The return of fundamental-based traders will add discipline to the price discovery process. It will allow the relationship between oil prices and global inventories to reassert itself, allowing prices to move higher.

Conclusion

Trump won, and conditions are ripe for change, from the regulatory front to the long-term production outlook. Energy stocks are already moving in unpredictable ways. It’s only a matter of time before a new juicy opportunity arises in the confusion created by a Presidential transition. Rest assured that we’re on the hunt. We’ll publish a write-up as soon as we find one.